Blog

Best Place to Finance Furniture with Bad Credit A Guide

You find the right sofa, a sturdy dining set, or a bed that would finally let you sleep without waking up stiff. Then the financing question shows up and changes the mood fast. If your credit has taken a few hits, that moment can feel personal, even though it happens to a lot of good people for a lot of ordinary reasons.

In Central Maine, that stress often lands all at once. A family moves into a new place in Augusta. A renter in Skowhegan needs to replace worn-out hand-me-down furniture. A new homeowner realizes empty rooms don't feel much like home. The need is real, but the financing offers can be hard to sort through.

The best place to finance furniture with bad credit usually isn't the place with the loudest promise. It's the place that helps you understand the terms, protects your budget, and gives you a realistic path to ownership. That's what this guide is for.

Table of Contents

- Making a House a Home in Maine Even with Credit Hurdles

- Why Bad Credit Can Complicate Furniture Buying

- A Guide to Common Bad Credit Financing Options

- Comparing Lease-to-Own Loans and Store Cards

- How to Prepare Your Application and Boost Approval Odds

- The Northern Advantage A Local Solution for Central Maine

Making a House a Home in Maine Even with Credit Hurdles

A lot of folks around here know this feeling. You're standing in a showroom or scrolling late at night after work, trying to figure out how to turn a bare room into something comfortable. You aren't shopping for luxury for luxury's sake. You're trying to make your place livable.

In Central Maine, furniture often comes into focus during big life changes. A move, a divorce, a growing family, a fresh start after a rough stretch. The couch matters because it's where the kids pile in for movie night. The bed matters because better sleep helps everything else go a little smoother. If you're setting up a home for the first time, this practical guide for getting organized from the start in a new home can help you think through the basics room by room.

Home needs don't wait for a perfect credit score

Bad credit can make ordinary purchases feel heavier than they should. People start wondering if they'll be judged, denied, or pushed into something they don't fully understand. Most of the time, they just want someone to explain the options in plain English.

That's especially true when furniture isn't a want. It's a need. A real dining table, a dependable recliner, a mattress that supports your back, or a durable sofa from a trusted brand like Ashley or Flexsteel can change how a home feels day to day.

You don't need perfect timing to build a comfortable home. You need a clear path and terms you can live with.

A local way of thinking about the problem

Around Augusta and Skowhegan, people tend to appreciate straightforward advice. No drama. No shame. Just a solid look at what works, what costs more than it first appears, and what questions to ask before signing anything.

That matters because the best place to finance furniture with bad credit isn't always a national chain with a flashy ad. Sometimes the better option is the one that treats you like a neighbor, answers your questions without pressure, and helps you invest in your home one good decision at a time.

Why Bad Credit Can Complicate Furniture Buying

Credit trouble doesn't always come from reckless spending. Sometimes it comes from job changes, medical bills, a thin credit file, or a period where everything got more expensive at once. Still, when you apply for financing, the system doesn't read your full story. It reads risk.

That can feel unfair, but it helps to know what lenders are usually looking for. Once you understand that part, the process gets less mysterious and a lot easier to manage. If you want a broader primer before you shop, this smart furniture shopping guide is a helpful companion.

What lenders are really asking

A lender usually wants to know a few basic things.

- Can you repay on time. They look for signs that your bills are manageable compared with your income.

- How have past accounts gone. A low score can signal missed payments, heavy balances, or short credit history.

- How stable is your current situation. Employment, banking history, and steady income can matter just as much as the score itself with some programs.

A FICO score is one common credit score lenders use. You don't need to memorize the formula. What matters is that lower scores often trigger stricter terms or automatic denials from traditional financing programs.

Why furniture gets treated like risk

Furniture financing sits in an awkward middle ground. The purchase is important to your daily life, but many traditional lenders still treat it as nonessential compared with a car or mortgage. That means they may be less flexible, especially if the application doesn't fit their usual credit profile.

When that happens, shoppers often run into one of these outcomes:

- A denial from standard retail credit

- An approval with expensive terms

- A redirect to an alternative lender that looks beyond the score

Practical rule: If a financing offer sounds easy but no one explains how ownership works, stop and ask more questions.

The confusion usually starts with the monthly payment

People often get tripped up. They see a weekly or monthly payment that feels manageable, and they assume the whole deal must be manageable too. But the payment alone doesn't tell you whether you're getting a loan, a lease, a store card, or a short-term installment plan.

Those products work differently. Some give you ownership right away. Some don't. Some may use a soft pull at first. Others may involve a hard inquiry. Some are built for a single purchase. Some are revolving credit.

That's why bad credit complicates furniture buying. Not because you have no options, but because the options get more layered, and the wrong fit can cost you more than you expected.

A Guide to Common Bad Credit Financing Options

A lot of Central Maine shoppers hit the same moment. You find the bed or sofa your home needs, then the financing choices start sounding like a different language. Loan. Lease. Store card. Pay-in-4. The names are familiar, but the fine print can lead in very different directions.

The simplest way to sort them is to ask one question first: Are you borrowing to buy, or paying over time before you own? That one question clears up a lot of confusion.

If you want a basic example of how payments can be structured, this guide to monthly payments on furniture can help.

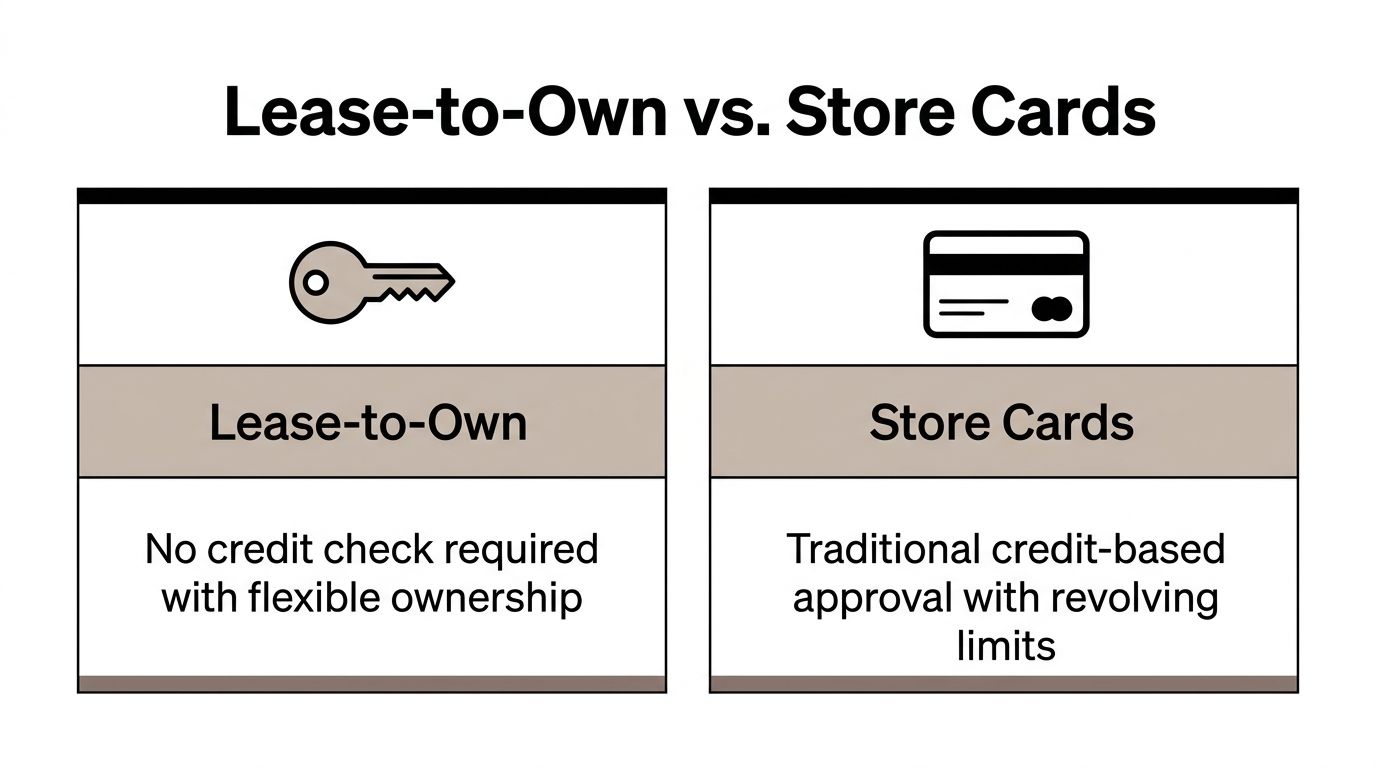

Lease to own

Lease-to-own works a lot like a long purchase path with ownership at the end instead of the beginning. You pick the furniture, apply through a leasing partner, and make scheduled payments. In many cases, the item does not belong to you until the agreement is completed or you use an early purchase option, if one is offered.

For people with bruised credit, this option can be more accessible because approval may depend more on income, banking history, and basic application details than on a traditional credit score alone.

Lease-to-own often fits shoppers who:

- Need furniture soon after a move, separation, or sudden household change

- Have been turned down for standard retail credit

- Want a payment plan they can understand clearly before signing

The tradeoff is cost. A low weekly payment can feel manageable in the same way a small leak under the sink seems manageable. Left alone, it adds up. That is why the full amount paid over time matters more than the first payment quoted at the counter.

Buy now pay later

Buy now pay later, or BNPL, breaks the purchase into smaller installments. Some plans are short, such as four payments. Others stretch longer and may charge interest depending on the provider and the terms offered.

This can work well for a modest purchase, such as a recliner, mattress, or one-room update. It gets harder to manage when several plans are running at once. A shopper may remember the sofa payment and forget the lamp, rug, and bedroom set are all due from different apps in the same month.

Another point to watch is the credit check. Some providers start with a soft pull for prequalification, while others may use a hard inquiry if you move ahead with the full application.

Personal loans and second look lenders

A personal loan is more straightforward. The lender gives you a set amount, you buy the furniture, and you repay the lender in fixed installments. Ownership starts right away because you purchased the item upfront.

Some lenders also offer what shoppers often call second-look financing. That usually means the application gets reviewed with more than a score in mind. Income, job stability, and checking account activity may carry weight.

This can be a better fit for someone who wants clear ownership from day one and prefers one fixed payment schedule instead of several smaller plans.

Store financing and in house options

Some furniture stores offer financing through a store card. Others work with several outside partners. Some local stores can also point you toward options that start with no-impact prequalification, which gives you a chance to see possible offers before a hard inquiry enters the picture.

That local piece matters more than many shoppers expect. A large national chain may hand you one financing path and leave you to sort out the rest alone. A trusted local store in Central Maine is more likely to slow the process down, explain whether the offer is a lease or a loan, and answer the questions people are sometimes embarrassed to ask.

Before you sign anything, ask:

- Is this a lease, a loan, a store card, or a short installment plan?

- When do I own the furniture?

- What is the full amount I may pay by the end?

- Does the first application use a soft pull or a hard pull?

- Are there fees, early purchase options, or missed-payment penalties?

- Can this be used for special orders or only in-stock items?

A good financing option should make your home more comfortable, not leave you guessing about what you agreed to. The best help usually comes from people who explain the terms in plain English and treat you like a neighbor, not a credit score.

Comparing Lease-to-Own Loans and Store Cards

A lot of Central Maine shoppers reach this point with one simple question: which option gets the couch, mattress, or dining set home without creating a bigger problem three months from now?

That is the right question.

The best place to finance furniture with bad credit is usually not the place with the loudest approval promise. It is the place that explains the agreement clearly, lets you compare real costs, and treats you like a neighbor who deserves straight answers.

National financing brands often present several products under one broad label. That can make very different agreements look similar at first glance. A lease-to-own plan, a personal loan, a BNPL plan, and a store card may all help you bring furniture home, but they do not work the same way once the paperwork starts.

If you want a closer look at how lease programs are typically explained, this guide to leasing furniture with no credit check shows what shoppers should look for before signing.

Bad Credit Furniture Financing Options at a Glance

| Financing Option | Best For | Typical Credit Impact | Potential Total Cost |

|---|---|---|---|

| Lease-to-own | Shoppers who need furniture now and may not qualify for standard credit | Often based less on traditional credit and more on income or banking history | Can be much higher than retail price over the full term |

| BNPL | Smaller purchases or shoppers who want split payments | Often starts with a soft review, depending on provider | Can stay manageable, but stacked plans can strain the budget |

| Personal loan | Shoppers who want fixed terms and immediate ownership | Depends on lender and application method | Varies by lender and credit profile |

| Store card or retail financing | Shoppers who may qualify for store-based credit and want one retailer-based solution | Often more credit-sensitive than lease programs | Can be reasonable or expensive depending on terms and payoff behavior |

How the options differ in real life

Here is the plain-English version. Lease-to-own is usually about access first. Store cards are usually about whether your credit file meets the lender's standards. Personal loans are often the most familiar structure. BNPL is often the simplest at checkout, but only if the purchase stays modest and the payment schedule stays manageable.

The easiest way to sort them out is to picture four different roads to the same living room set. You may arrive at the same sofa, but the tolls, the timing, and the rules of the road can be very different.

Ownership path

With a personal loan or store card, you usually buy the furniture right away and own it from day one. With lease-to-own, you usually make scheduled payments over time and ownership comes later if you complete the agreement or use an early purchase option.

That distinction matters more than it sounds. If a table breaks, if you want to move, or if you want to pay everything off early, your rights and options can look very different depending on whether you already own the item.

Approval style

Lease programs and other second-look options often pay closer attention to practical signs of stability, such as income, account activity, and consistent information on the application. Store cards usually rely more heavily on the credit report.

This is one reason a local store can be easier to work with than a large chain. A national site may send you into an automated application flow and leave you to sort out the fine print alone. A well-known Central Maine business is more likely to explain which path starts with no-impact prequalification, which one may involve a hard inquiry, and which option fits your budget instead of just your approval odds.

Cost over time

Many shoppers get tripped up at this stage.

A low weekly payment can feel manageable in the moment. A small minimum payment on a store card can look harmless too. But payment size is only one piece of the puzzle. The essential question is the full amount paid by the end of the agreement.

As noted earlier in the article, lease-to-own can cost much more than the cash price over the full term. Store cards can also become expensive if the rate is high or the balance lingers. The safest approach is to compare the total cost, not just the payment that gets advertised on the sign or screen.

If the monthly or weekly payment looks comfortable, but the full payoff amount would make you hesitate, stop there and ask more questions.

The question that saves people money

Ask this before signing:

What is the total amount I will pay if I follow this agreement all the way through?

That one sentence clears up a lot of confusion. It helps you compare a lease against a store card, a loan against BNPL, and a quick approval against a better long-term fit.

Here are the trade-offs in plain terms:

- Choose lease-to-own when getting the furniture now matters most and traditional credit approval may be less likely.

- Choose a personal loan when you want a fixed schedule and ownership from the start.

- Choose BNPL when the purchase is smaller and you are confident you will not stack multiple payment plans at once.

- Choose a store card when you understand the rate, the terms, and the effect it may have on your credit profile.

For many Maine households, the best answer is the option that still makes sense after the excitement of delivery day has passed. A supportive local store should help you reach that answer without pressure or judgment.

How to Prepare Your Application and Boost Approval Odds

A better application starts before you sit down in the showroom or click the first prequalification button. Most denials don't feel informative in the moment, but a lot of them come down to missing paperwork, mismatched information, or applying for more than your budget comfortably supports.

This stage is where preparation helps you feel more in control. If you want a broader look at how people move from browsing to buying, this article on the furniture buying journey from first research to final decision lays that process out clearly.

Get your paperwork together first

Bring the basics, even if you're applying online.

- Proof of income. Recent pay stubs or benefit statements can show stable income.

- Valid identification. Name and address issues can slow things down quickly.

- Banking information. Some lenders or lease providers want to verify an active checking account.

- Proof of address. A utility bill or lease can help if your current address is new.

- A realistic purchase list. Know which pieces you need now and which can wait.

Don't overlook accuracy. If your income, job history, or address doesn't match across documents, some systems flag the application for review or reject it outright.

Apply with a plan not just hope

Start with the furniture that matters most. A bed you need for better sleep is more important than stretching for a whole-house package. A durable sofa for daily use matters more than decorative extras.

That doesn't mean thinking small forever. It means choosing a cleaner first step.

Try this checklist before you apply:

- Set a true payment limit. Pick a number that still leaves room for groceries, utilities, gas, and the usual surprises.

- Know your must-haves. Separate urgent items from things you want.

- Ask how the application works. Is it prequalification, a soft pull, a hard inquiry, or a lease review.

- Have a down payment ready if possible. Even a smaller upfront contribution can make the deal easier to manage.

- Ask about custom orders. If you need a particular size, fabric, or configuration, make sure the financing path works for that purchase too.

Bring your room measurements, your monthly budget, and your questions. That combination is more useful than optimism alone.

In-person applications can also help when you're confused about terms. A knowledgeable associate can sometimes explain the difference between a lease, a loan, and a store card far better than a generic checkout screen can.

The Northern Advantage A Local Solution for Central Maine

For Central Maine shoppers, the strongest financing experience often comes from a local store that understands the rhythm of the community. Rural distance, limited chain options, and the need to talk with a real person all shape the decision more than national ads admit.

According to American First Finance's discussion of bad credit furniture financing, national lease-to-own options dominate search results, but they often miss rural accessibility gaps. The same source notes that local stores can help people overcome digital-only hurdles, especially new movers and shoppers with less-than-perfect credit, and it points to CFPB scrutiny around repossession risk in national rent-to-own models.

Why local help matters in rural Maine

The Central Maine perspective is especially relevant. In Augusta or Skowhegan, plenty of shoppers would rather sit down, ask questions, and understand what they're signing. They don't want a faceless approval screen. They want clarity.

A local, third-generation family business that has served the area since 1950 brings something national chains can't fake. Familiarity. Accountability. A reputation that has to hold up over time.

That kind of setting also helps if your purchase isn't simple. Maybe you want a durable Flexsteel sectional in a custom fabric. Maybe you need an Ashley bedroom set that fits a tighter room. Maybe you don't want to settle for whatever happens to be on the floor because you're making a house a home and you want it to feel like yours.

What a better financing experience looks like

A better local option combines three things:

- Straightforward pricing. Real Sale Prices matter more than flashy markdown language. A Price Chop promise means more when you're already watching every dollar.

- Flexible choices. A Custom Order program gives you access to styles, fabrics, and configurations beyond floor models.

- Low-pressure financing. The Nest Credit Card lets shoppers pre-qualify with no impact to their credit score, which matters a lot when fear of another rejection is the biggest barrier to even asking.

The in-store experience matters too. No-hassle help, experienced associates, and simple comforts like complimentary coffee and bottled water can make a stressful decision feel manageable again.

For many neighbors in Central Maine, that's the answer to the question. The best place to finance furniture with bad credit is a local showroom where people explain things clearly, offer practical options, and treat your budget with respect.

If you'd like a local, judgment-free place to start, visit Northern Mattress & Furniture 1st in Augusta or Skowhegan. You can explore durable furniture from trusted brands, ask about Custom Orders for the right fit in your home, and check Nest Credit Card pre-qualification with no impact to your credit score. It's a simple way to find the right fit, see Real Sale Prices, and invest in your home without the hassle.