Blog

Easy Furniture Financing for Your Central Maine Home

A lot of folks in Central Maine get to the same point around the same time. The house is working, but it isn't quite living the way they want it to. The old sofa has seen better days. The guest room still looks half-finished. The dining set doesn't fit how the family gathers now.

Then reality steps in. Furnishing a home is a real expense, especially when you're trying to do it thoughtfully instead of buying stopgap pieces that won't last through a few Maine winters.

That's where easy furniture financing can help, if you understand how it works before you sign anything. Used the right way, financing isn't about stretching your budget until it squeaks. It's about giving yourself room to choose durable pieces, plan delivery, and invest in your home without turning the purchase into a headache.

For families around Augusta, Skowhegan, and across Central Maine, that matters. A third-generation business that's been part of the community since 1950 can see the same pattern over and over. People want comfort, value, and straight answers. They don't want jargon. They want to know what the payment really means, when it starts, and what happens if the piece they want is a custom order instead of something going out on the truck this week. That's also why it helps to understand the full furniture buying journey from first research to final decision.

Table of Contents

- Making Your Dream Home in Maine a Reality

- Decoding Your Furniture Financing Options

- Check Your Eligibility Without Hurting Your Credit Score

- Matching Your Financing Plan to Your Purchase

- Navigating Common Financing Pitfalls

- Why Financing with a Local Family Business Matters

Making Your Dream Home in Maine a Reality

In Central Maine, home projects rarely happen in a perfect straight line. A family starts with one need, maybe a new mattress for better sleep or a sturdier sectional for the room where everyone lands after work and school. Then they realize the lamp tables need replacing too, or the dining space could work better before the holidays roll around again.

That's usually when the budget conversation gets real. Not because the purchase is a mistake, but because good furniture is part of making a house feel settled. It's part comfort, part function, part durability.

A practical way to buy what you need

Financing can be a sensible tool when you use it to match the purchase to your household budget. It gives you a way to bring home the pieces you need now, while spreading the cost into a payment schedule that feels manageable.

Some retailers build that flexibility into their programs. For example, Price Point Furniture's financing page shows in-store terms of 6, 12, 18, 24, or 36 months, plus Affirm options that split purchases into 3, 6, or 12 monthly payments. The same page also shows that eligibility-based APR can range from 0% to 36%, and one listed example includes a 39.99% penalty APR and a $2 minimum interest charge, which is a good reminder that easy financing is only easy when you understand the cost structure.

Financing should make the room easier to live with, not harder to pay for three months later.

Why this matters in Maine

Local shoppers often aren't furnishing just one room. They're balancing a whole-home plan. That might mean a recliner that lasts, a bedroom set that fits an older farmhouse, or a custom sectional that works in a camp, condo, or family room with awkward dimensions.

That's where a plain-English approach helps. If you're looking at durable brands like Ashley or Flexsteel, or you want something beyond the floor model through a custom order program, the financing conversation needs to be tied to the actual purchase. Not just a monthly payment on paper.

A neighborly store should help you sort through that without pressure. The no-hassle part matters. So does walking into a showroom in Augusta or Skowhegan, grabbing a coffee or bottled water, and having someone explain your options like a person, not a script.

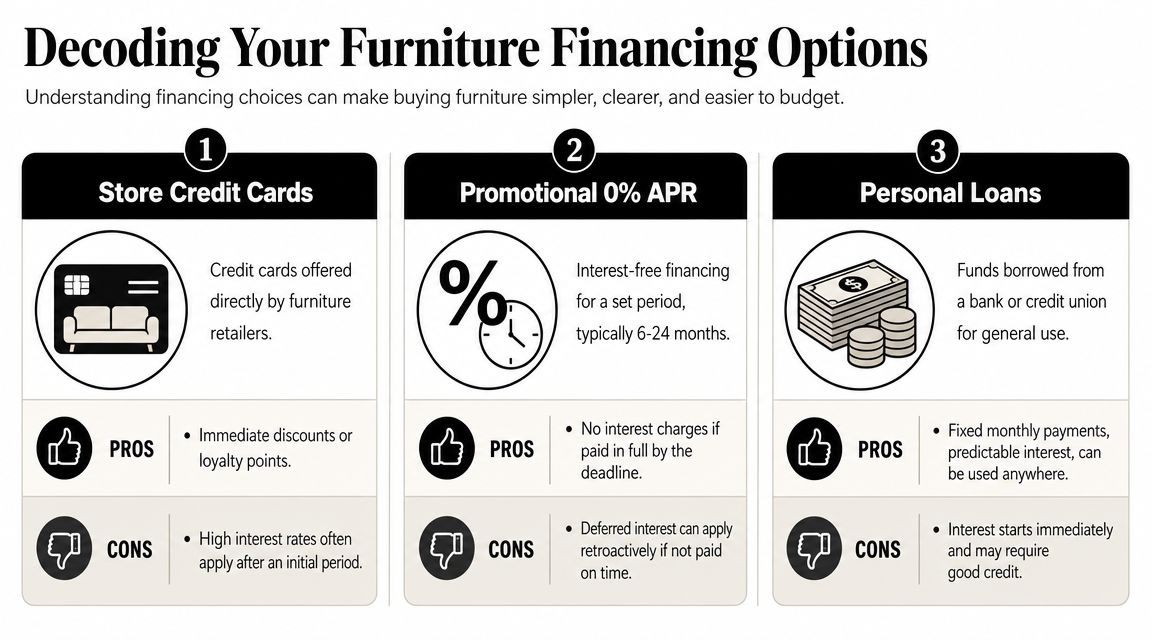

Decoding Your Furniture Financing Options

Most financing offers sound simple at first glance. Apply quickly. Get an answer fast. Take it home now. The hard part isn't getting the headline. The hard part is understanding what kind of financing you're being offered.

The main financing paths

Here's the plain-English version of the options most shoppers run into.

| Financing type | How it usually works | Best fit for |

|---|---|---|

| Store credit card | You apply through the retailer and, if approved, use that account for your purchase | Shoppers who want retailer-based promotions or repeat-use flexibility |

| Promotional APR offer | A set financing window may offer low or no interest for a period, depending on terms | Buyers with a payoff plan already in mind |

| Installment or BNPL plan | The purchase is split into scheduled payments over a shorter term | Smaller or mid-sized purchases where budget timing matters |

| Personal loan | You borrow a fixed amount and repay on a fixed schedule | Shoppers who want predictable payments and a separate financing source |

The appeal is flexibility. As noted earlier, easy furniture financing often comes with a range of term lengths instead of one rigid option. That makes it easier to fit a purchase into a real household budget.

Where the Nest Credit Card fits

A store card can be useful when you want one account tied to a furniture purchase instead of using a general credit card. The Nest Credit Card falls into that category. It's one example of a retailer-based option that lets shoppers look into financing for home purchases, and you can review the financing details here.

A few practical differences matter:

- Shorter plans can reduce exposure if you know the purchase is modest and you can pay it down quickly.

- Longer plans can ease the monthly strain on bigger-ticket rooms, but you need to check the full cost, not just the payment.

- Third-party installment tools can be convenient at checkout, though the terms may differ from a store card.

- Personal loans can be easier to budget because payments are often fixed from the start, but interest may begin immediately.

Practical rule: If you can't explain to yourself how the balance gets paid off, the offer isn't clear enough yet.

That's the ultimate test. Good financing should feel understandable. If a plan only sounds attractive because the monthly payment looks small, pause and ask a few more questions.

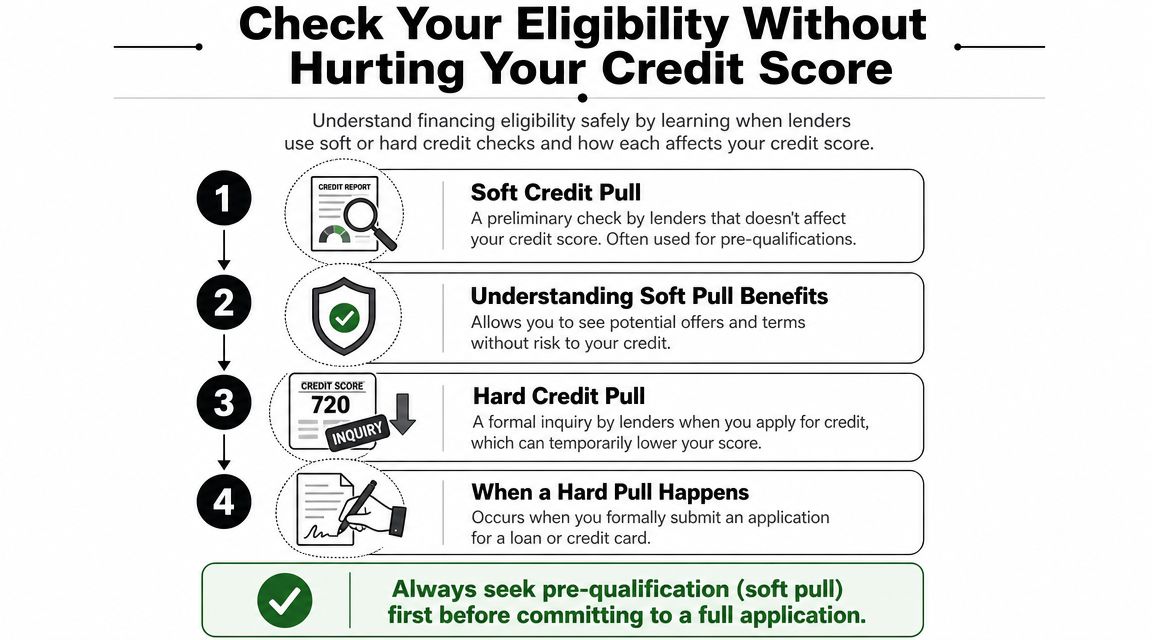

Check Your Eligibility Without Hurting Your Credit Score

The fear that stops a lot of people is simple. They want to see what they might qualify for, but they don't want to damage their credit just for asking.

That's a fair concern, and it's why prequalification matters.

Soft pull first, full application later

A soft pull is generally used for prequalification. It lets you check whether you may be eligible for financing without committing to the full application process. For shoppers, that means less stress and a clearer starting point.

A hard pull is different. That usually happens when you move into a formal credit application and the lender does a more complete review.

If you're trying to stay organized, the simplest path is this:

- Prequalify first so you can see whether an offer may be available.

- Review the term and payment structure before you decide anything.

- Submit a full application only when you're comfortable with the purchase and the agreement.

That's one reason many shoppers start with options that advertise no-impact prequalification. If you're comparing paths, this guide on buying furniture with no credit check is a helpful next read.

What lenders usually look at

Not every financing path uses the same approval standard. Traditional furniture lenders often look for a credit score of 620 or higher, while broader-access options may welcome all credit types and in some cases don't require any credit history at all, according to BadCredit.org's overview of furniture financing options.

That doesn't mean approval is automatic. It means the market has split into a few lanes.

- Traditional credit-based offers often work best for shoppers who fit standard lending criteria.

- Store cards and alternative programs may cast a wider net.

- Lease-to-own style offers can help shoppers who don't fit the usual credit profile, though the trade-offs need careful review.

A prequalification tool is for information. It's not a promise, and it's not a commitment. It's a safe way to get your bearings.

This is also where shoppers should stay practical. Approval by itself doesn't tell you whether the plan is a good fit. It only tells you the door is open. You still need to decide whether the payment, term, and product timing make sense for your household.

Matching Your Financing Plan to Your Purchase

You pick out a recliner that's sitting in the showroom, and it could be in your house by the weekend. You order a custom sectional in a specific fabric, and that piece may take quite a while to arrive. Both purchases can be financed, but they should not be financed with the same assumptions.

That's the part shoppers in Maine often appreciate once we talk it through. The financing itself may look similar on paper, yet the delivery timeline, the start date for payments, and the return terms can be very different depending on whether the piece is in stock or built to order.

In-stock pieces usually call for speed and clean math

With in-stock furniture, the goal is usually simple. Get clear on the total amount, confirm what is included, and make sure the payment fits your monthly budget before the item leaves the floor.

These purchases tend to move fast. A sofa, mattress, or dining set that is available now often comes with a shorter decision window because inventory changes and sale pricing may not last. That makes it smart to ask practical questions before you say yes, not after the paperwork is done.

For an in-stock purchase, focus on these details:

- How soon delivery or pickup can happen

- When the first payment is due

- Whether delivery, protection plans, taxes, or setup are part of the financed total

- Whether the monthly payment still feels comfortable after you account for the rest of your bills

Simple beats flashy here.

If the piece is going into daily use right away, a straightforward plan with clear terms often serves you better than chasing the longest offer without checking the full monthly cost.

Custom orders need a planning mindset

Custom furniture changes the decision because time becomes part of the cost. Fabric choice, configuration, sizing, and special-order options are worth it for many homes, but they add another layer to financing.

One of the biggest questions is when the financing agreement starts relative to the order and delivery timeline. Biz2Credit's discussion of financing inventory and furniture timing points to how order timing can affect cash flow. For a household buyer, that same timing matters because you may be making payments before the furniture ever reaches your living room.

Here's the checklist I'd use for a custom order in Central Maine:

- Ask when the financing term begins

- Confirm whether any promotional period applies during the wait time

- Read the cancellation and return policy carefully for made-to-order pieces

- Choose a term that still feels manageable if delivery takes longer than expected

- Make sure the purchase fits your broader room plan, not just today's payment

That last point matters more than people think. A custom sectional, bedroom set, or dining group is usually part of a bigger project, and this furniture shopping guide for planning a room smartly can help you sort through the decisions before you finance the wrong mix.

If you're ordering custom furniture, ask two questions early. When do payments start, and what happens if the delivery date shifts?

Those answers help you plan the whole purchase with fewer surprises. That's especially important in Maine, where many shoppers are furnishing not just one piece, but an entire room and trying to line up budget, timing, and delivery in a way that feels manageable.

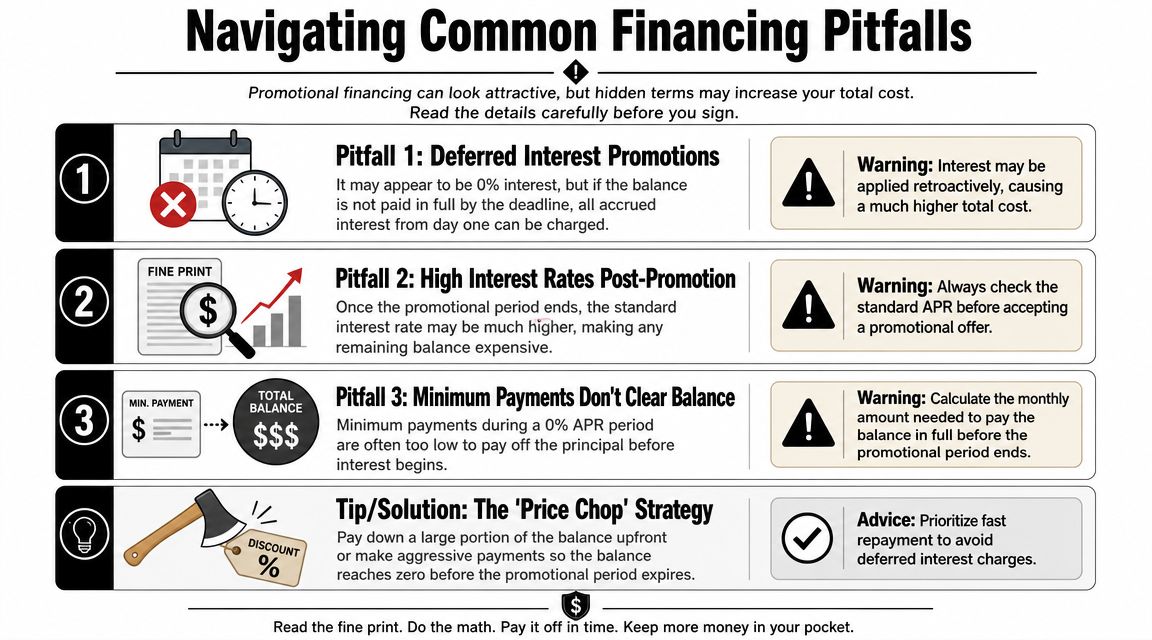

Navigating Common Financing Pitfalls

The most common misunderstanding in furniture financing is also the most expensive one. People hear 0% and assume the whole deal is simple.

Sometimes it is. Sometimes it isn't.

The fine print that changes total cost

Many promotional offers require the balance to be paid in full within the promo window. If it isn't, interest may be charged retroactively from the original purchase date. Guidance from Guynn Furniture's financing overview notes that this is a major pitfall with many 0% APR offers, and that promotional periods commonly run from 12 to 60 months in the example discussed there.

Shoppers often get tripped up. The monthly payment can look gentle, but the structure may not be forgiving if you're still carrying a balance at the end.

A safer way to compare offers

Instead of asking only, “What's the monthly payment?” ask these:

- Is this true 0% APR or deferred interest

- What amount do I need to pay each month to finish on time

- What rate applies after the promotion

- Are late fees, penalty terms, or other charges spelled out clearly

That kind of comparison fits well with a value-minded approach. “Real Sale Prices” and an honest Price Chop promise mean more when the financing side is just as clear as the furniture price.

For shoppers working through tougher credit questions, this article on where to finance furniture with bad credit adds some practical context.

Minimum payments and payoff payments are not always the same thing.

One more thing stores don't always spell out clearly. Approval speed isn't the same as affordability. Easy furniture financing works best when the monthly number fits your real life, not just your checkout moment.

Why Financing with a Local Family Business Matters

You pick out a sofa on Saturday, then realize the version that fits your room best has to be custom ordered. Now the question is not only whether the payment works. It is whether the financing timing, delivery window, and order details all line up cleanly.

That is where a local family business earns its keep.

At a store that has served Central Maine since 1950, the financing conversation tends to stay connected to the overall project. Staff are not only looking at an application screen. They are also helping sort out room measurements, fabric choices, stair clearance, daily wear, and whether you are buying something you can take home soon or something that will arrive later as a custom order. For Maine households, that matters. In-stock pieces and custom pieces do not move on the same timeline, and your payment plan should make sense for the one you are buying.

Local guidance changes the experience

A good financing process is straightforward. You fill out the application, review the terms, confirm what the payment schedule looks like, and understand when the furniture is expected to be available.

The local advantage is that the same conversation can cover the product and the financing at once.

- In-stock furniture is often about quick decisions, delivery scheduling, and making sure the monthly payment fits before the piece comes home.

- Custom-ordered furniture needs more planning. You want clear expectations on lead times, deposits, and when financing begins, so there are no surprises while you wait for the order to arrive.

- Quality matters because financing a piece that wears out too soon usually feels expensive later, even if the payment looked manageable at checkout.

That kind of guidance is hard to fake. It comes from people who know the furniture, know the ordering process, and understand how families in this area shop.

What that looks like in Augusta and Skowhegan

In practical terms, local service gives you room to slow down and make a sound decision. You can sit on the sofa, open the drawers, compare fabrics, ask what is stocked now versus what needs to be ordered, and talk through payment options with someone who can answer the next question too. That lowers stress.

It also helps you avoid a common mistake. Shoppers sometimes finance based on the piece they first saw on the floor, then switch to a different configuration, fabric, or bedroom group without stopping to revisit timing and total cost. A good local store catches that before it turns into confusion.

That is part of why many Central Maine shoppers prefer working with a business they can visit in person. Clear answers matter. So does accountability.

If you're planning a room refresh, replacing worn-out basics, or ordering something custom for your home, Northern Mattress & Furniture 1st is a practical place to start. You can browse styles, compare financing options, and visit the Augusta or Skowhegan showrooms for a no-pressure conversation about what fits your space, your budget, and your timeline.