Blog

Buy Furniture No Credit Check | Your 2026 Guide

A lot of people start looking up buy furniture no credit check when the need is immediate. The old sofa has given out, guests are coming, the mattress is wrecking your sleep, or you're moving into a place that still feels half empty. The furniture need is real. The stress around financing is real too.

Around Central Maine, I've seen the same concern come up again and again. People don't want to get boxed into a bad deal just because they need a bed, a recliner, or a dining set now. They want a straight answer on what the options are, what the full cost looks like, and how to avoid making a hard situation more expensive.

That's the right instinct. There are ways to furnish your home without a hard credit inquiry, but not every path works in your favor. Some plans are reasonable for the right shopper. Others look easy upfront and turn into a costly long-term commitment.

If you care about your budget, your home, and your peace of mind, the smart move is to understand the full picture before signing anything.

Table of Contents

- The Maine Connection Furnishing Your Home Without the Worry

- Exploring Your No Credit Check Furniture Options

- How to Prepare for a Smooth Approval

- Understanding the Real Cost of No Credit Check Furniture

- A Smarter First Step The Soft Pull Prequalification

- Making Your House a Home with Confidence

The Maine Connection Furnishing Your Home Without the Worry

In Central Maine, home life changes with the season. Fall means family visits. Winter means you notice every sagging seat cushion and every mattress that no longer supports you. Spring often brings moves, fresh starts, and the urge to finally make a house feel settled.

That's why financing questions can feel personal. If you're trying to buy furniture no credit check, you're usually not chasing luxury. You're trying to solve a practical problem without adding more stress to your month.

As a third-generation family business serving Augusta, Skowhegan, and the surrounding area since 1950, we've learned that our customers want the same thing. They want clear choices, honest pricing, and enough breathing room to make a thoughtful decision. They don't want to be embarrassed about credit, and they don't want a rushed answer.

A furniture purchase should help your home function better. It shouldn't leave you confused about what you actually agreed to pay.

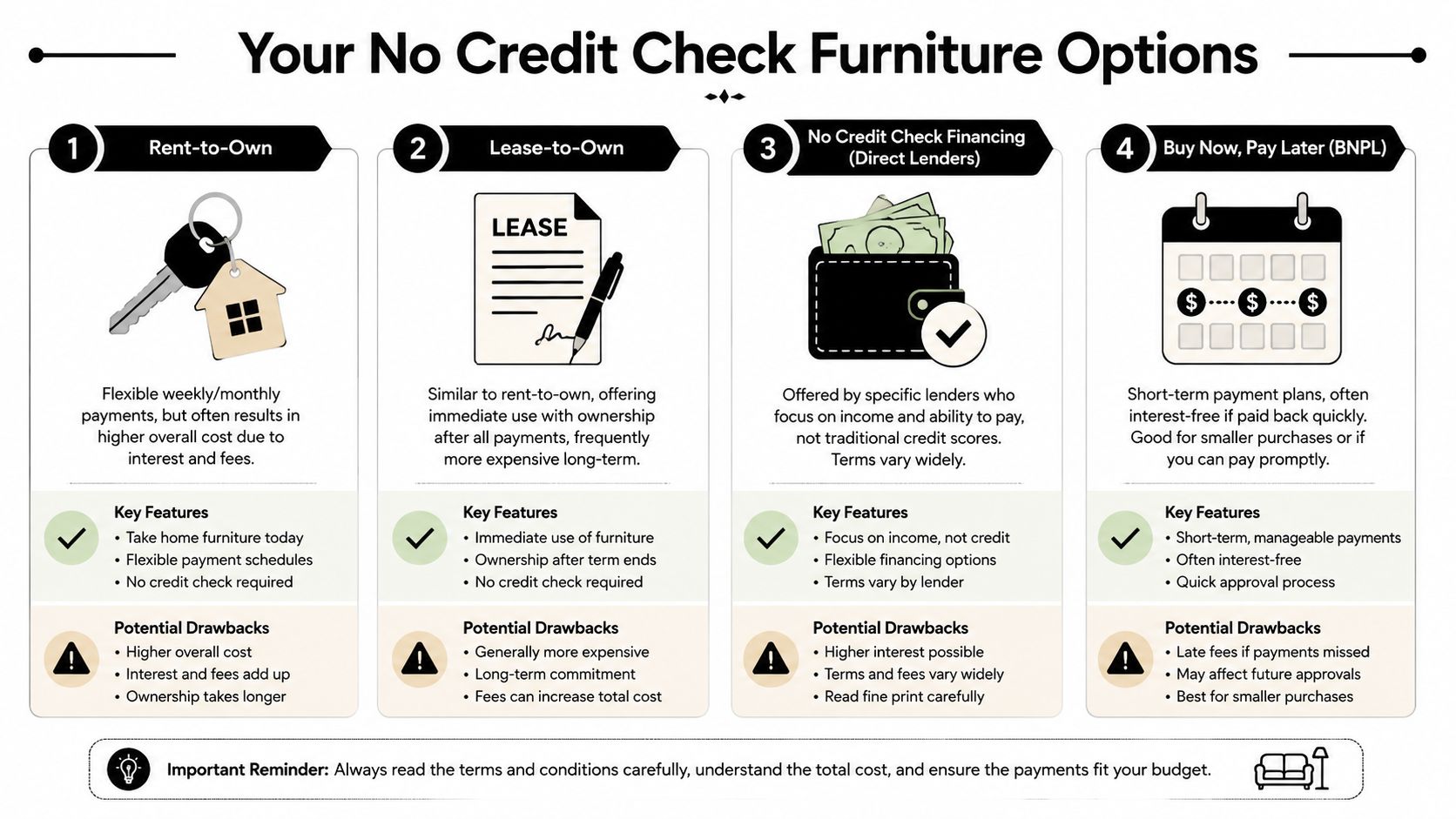

There are a few common ways these programs work. Some let you take the furniture home right away and pay over time. Some are structured like leases. Others use alternative approval methods instead of a traditional credit decision. Some delay delivery until you've paid in full.

The key is knowing which kind of agreement you're looking at before you focus on the monthly payment. That one habit protects people from a lot of regret.

If home comfort has been tied to stress lately, this perspective on loving your space as a form of self-care is worth a read too. A better home setup matters. It just needs to be done with clear eyes.

Exploring Your No Credit Check Furniture Options

Some shoppers assume “no credit check” means there's only one kind of financing. In practice, there are several models, and they don't work the same way.

What these programs usually look at instead of credit

No-credit-check furniture programs often rely on alternative underwriting rather than a traditional credit score. That can include income verification, employment history, and banking activity. Common minimum requirements include proof of at least $1,000 monthly income and an active checking account, and the market includes lease-to-own programs, BNPL apps, and store-specific credit options, as outlined in Biz2Credit's overview of no-credit-check furniture financing.

Here's how the main options tend to work in plain English:

- Lease-to-own or rent-to-own: You take the furniture home right away and make scheduled payments over time. You usually don't own the item until all required payments are complete. This can help when credit is limited, but the total paid can be much higher than the ticket price.

- Buy Now Pay Later: These plans are often simpler and shorter-term. They can work well for smaller purchases if the payment window fits comfortably in your budget.

- Store programs using nontraditional approval: Some retailers work with providers that focus more on current income and bank activity than on a FICO score.

- Layaway: This is the slowest option, but also the most straightforward. You make payments before taking the furniture home, which can help people avoid taking on a larger long-term obligation.

Practical rule: Before you compare payment amounts, ask one question first. “Do I own it today, own it after payoff, or only after completing a lease?”

What to bring before you apply

Walking in prepared makes the process much easier. Even if the approval process is fast, it still goes smoother when you have your details ready.

A practical file usually includes:

- Photo ID: A current government-issued ID helps verify identity quickly.

- Income proof: Pay stubs or similar records help show that the payment fits your current situation.

- Banking information: Many programs want to confirm an active checking account.

- Employment details: Basic employer information is often part of the review.

- Contact references: Some applications ask for personal references as part of identity and stability verification.

If you want a simple primer on financing questions before you visit a store, this guide to monthly payments on furniture gives a helpful starting point.

How to Prepare for a Smooth Approval

A smooth approval usually has less to do with luck and more to do with preparation. When lenders skip a traditional score, they still need another way to judge whether the account makes sense. That's why these applications tend to focus on current ability to pay instead of older credit history.

Why preparation matters

No-credit financing often looks at proof of income, banking history, and employment stability. Approval rates can reach 60-85%, many programs request only 2-4 personal references, and providers such as Acima and Snap Finance may approve up to $5,000, according to Las Vegas Furniture Online's breakdown of no-credit furniture financing.

That sounds encouraging, but approval alone isn't the finish line. The best outcome is getting approved for something you can carry comfortably without pinching your budget every month.

A rushed shopper usually focuses on one question: “Can I get it?” A prepared shopper asks better ones:

- What's the full payoff amount?

- When is the first payment due?

- What happens if a payment is late?

- Is this a lease, a loan, or a promotional financing plan?

- Are there conditions that change the price later?

Bring the paperwork that proves your situation today. That's what these programs are usually evaluating.

A simple approval checklist

Use this before you apply in-store or online:

| Item | Why it matters |

|---|---|

| Valid ID | Confirms identity and speeds up the application |

| Recent income proof | Shows current ability to make payments |

| Active checking account info | Often needed for verification and payment setup |

| Employer details | Supports employment stability review |

| Personal references | Some programs use these instead of deeper credit review |

One more step matters just as much as documents. Write down your own spending limit before you shop. Not the lender's limit. Yours.

That number keeps you grounded when you fall in love with a larger sectional, a power recliner set, or a bedroom package that stretches beyond what feels comfortable. Financing should support your home. It shouldn't reshape your whole monthly budget.

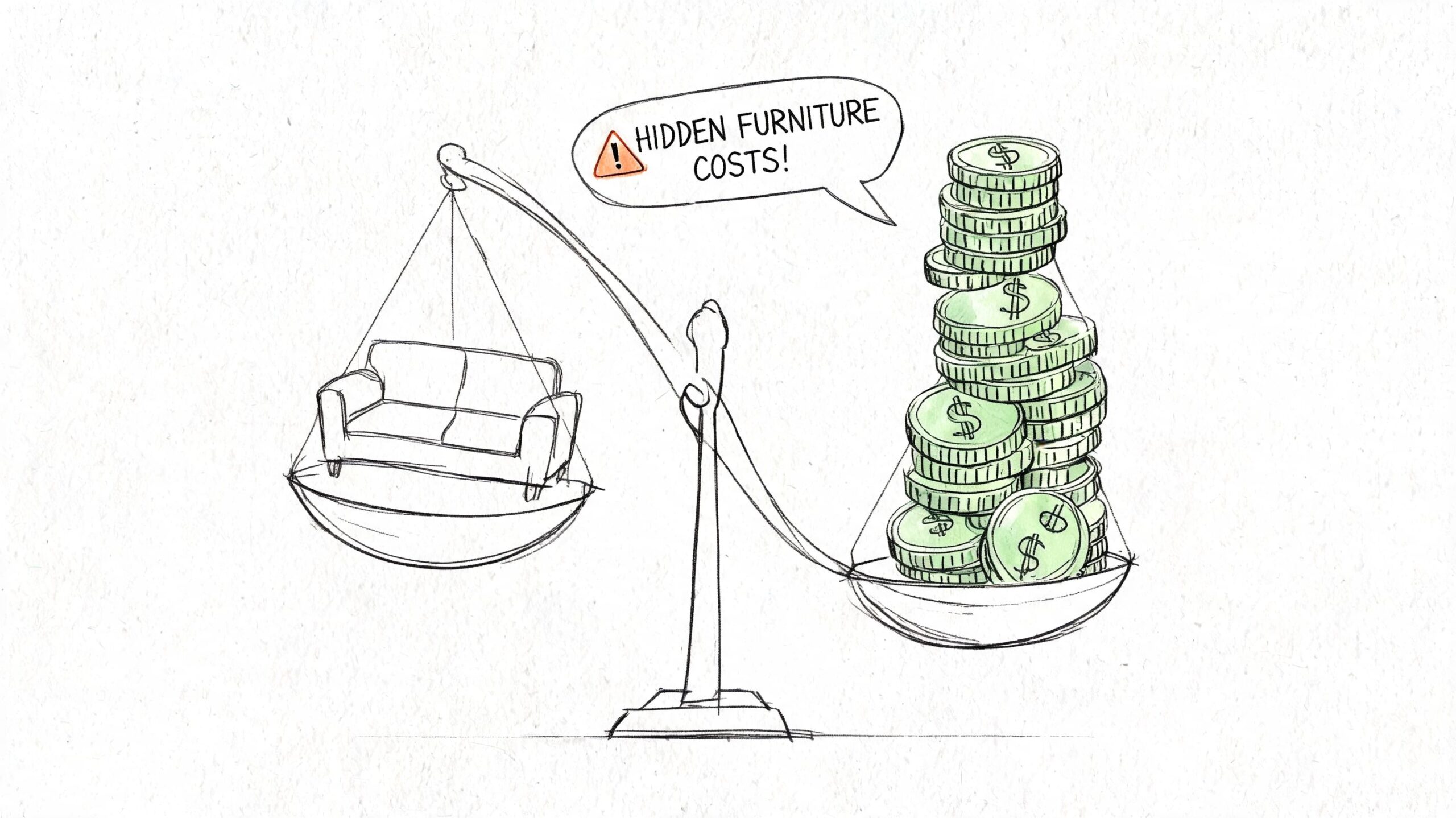

Understanding the Real Cost of No Credit Check Furniture

Monthly payment language can hide the actual price of furniture. That's the issue I want shoppers to understand before they sign anything. If you only look at whether the payment fits this week, you can miss what the agreement costs over the full term.

Why total cost matters more than the monthly payment

Traditional credit financing for furniture may run at 8-15% APR, while no-credit financing can reach 20-29.99% APR. Rent-to-own agreements can push the total paid to 2-5 times the retail price. One example from Pierce Furniture Gallery's financing comparison shows a $3,000 bedroom set at 25% APR over 24 months costing about $4,650 total.

That's the heart of total cost of ownership. The sofa, bed, or dining set has one sticker price. The financing path may create a very different final price.

Here's a simple way to evaluate any offer:

- Start with the cash price: What does the item cost before financing?

- Ask for the total of payments: Not the monthly amount alone.

- Check whether you own the furniture immediately or only after payoff

- Read the trigger points: Promotional periods, missed-payment terms, and any fee language matter.

If a retailer or financing partner can't clearly tell you the full payoff amount, slow down.

There's a reason furniture purchases are careful decisions for most households. This look at why furniture purchases are high-consideration decisions reflects that reality well. You live with the product, and with the financing choice, for a long time.

Why soft pull should come first

When no-credit options carry that kind of pricing risk, the smartest first move is to check whether you qualify for a lower-cost path without risking damage to your score. That means soft-pull prequalification deserves to happen before lease-to-own or high-APR agreements enter the conversation.

I'd put it this way. If a no-impact check can tell you whether a better financing path is available, skipping that step doesn't make much sense. It's a low-risk way to gather facts before you commit to a higher-cost structure.

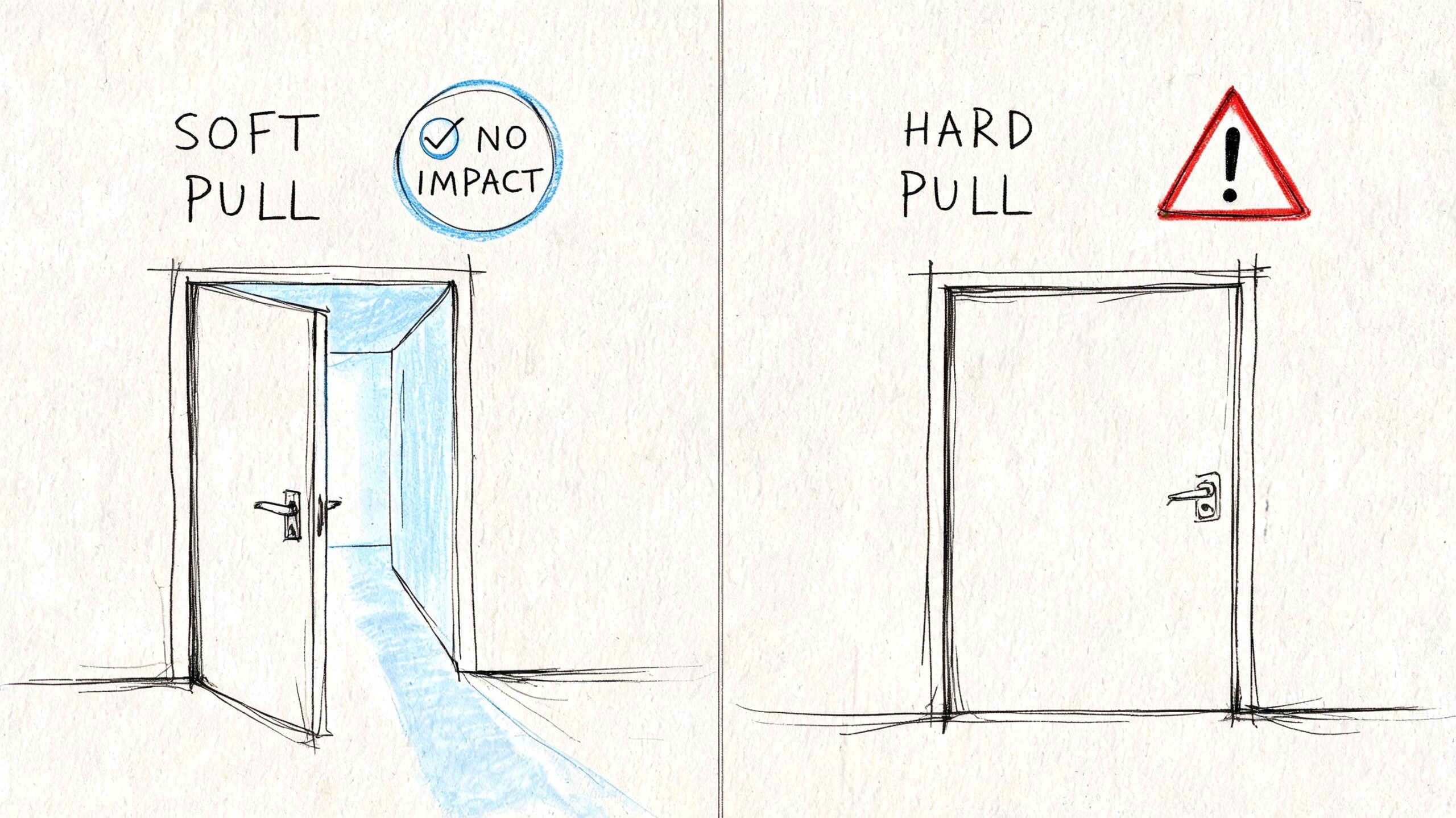

A Smarter First Step The Soft Pull Prequalification

Most shoppers hear “credit check” and assume every financing application will leave a mark. That's not always true. A soft pull is different from a hard inquiry, and that difference matters when you're trying to protect your options.

What makes a soft pull different

Many no-credit-check furniture programs carry post-promotional APRs of 25% to 29%, while traditional loans commonly require a credit score around 650. That pricing gap is exactly why Miller Waldrop's review of furniture financing for bad credit points to soft-pull prequalification as an important first step when better terms may be available.

That's the practical advantage. You get information first.

A soft pull can help answer questions like:

- Am I eligible for a standard financing path instead of a no-credit lease model?

- Could I qualify for promotional financing instead of a high post-promotional APR?

- Should I keep comparing options before I commit?

One factual example in the market is the Nest Credit Card, which offers prequalification without credit score impact. That makes it useful as an early filter before someone agrees to a more expensive no-credit structure.

How this fits real furniture shopping

This approach works especially well when the furniture itself is a long-term purchase. A durable sofa from Ashley or a seating upgrade from Flexsteel isn't something most families want to replace quickly. If you're investing in your home, the financing decision should be as carefully chosen as the frame, fabric, and cushion support.

A soft pull also fits the way thoughtful shoppers buy. You can check where you stand, compare the actual terms available to you, and then decide whether it makes more sense to finance, use layaway, scale the purchase down, or custom order something that better fits your budget and room.

If you're comparing styles and specifications at the same time, this guide to reading furniture product descriptions with confidence helps you evaluate the product side with the same level of care.

The safest financing step is often the one that gives you more information without locking you into a costly agreement.

Making Your House a Home with Confidence

Furniture financing matters, but the reason you're doing any of this is simple. You want a home that works. You want a bedroom that helps you rest, a dining room that gets used, and a living room where people want to sit down and stay awhile.

That's why I always come back to durability and fit. A lower payment on furniture that won't hold up isn't much of a win. Better to choose pieces that make sense for your life, whether that means a solid reclining sofa, a well-built bedroom set, or a mattress that improves sleep instead of just checking a price box.

In Central Maine, people also want flexibility. Sometimes the right answer is an in-stock piece at a real sale price. Sometimes it's a custom order in a different fabric, finish, or configuration so the furniture fits your room and the way you live. That's part of making a house a home. You're not limited to whatever happens to be on the floor that day.

The same goes for price. Real value means looking past flashy promotions and asking what you're getting, what you'll pay over time, and how long the piece should serve your family. That's where reputable names like Flexsteel and Ashley earn trust.

If you've been trying to make your home feel more settled, this piece on creating space you love and share is a good reminder that comfort and connection matter just as much as square footage.

If you'd like to talk through your options in a low-pressure way, visit Northern Mattress & Furniture 1st in Augusta or Skowhegan. You can browse, ask questions, compare financing paths, look at custom-order possibilities, and take your time. There's no-hassle support, complimentary coffee and bottled water, and a team that's been part of the Central Maine community since 1950.