Blog

What Is a Soft Pull Credit Check: No Credit Score Impact

A lot of Central Maine families reach the same point at about the same time. The sofa has seen one too many muddy boots. The guest room still doesn't feel finished. The mattress that seemed “good enough” a few years ago now feels like the reason sleep isn't coming easy.

Then financing enters the picture, and so does hesitation.

For many shoppers in Augusta, Skowhegan, and the surrounding towns, the worry isn't just the monthly payment. It's the credit check. People hear terms like “soft pull,” “hard pull,” and “prequalification,” and the whole thing can start to sound more intimidating than it really is. That's especially true when someone is trying to make a house a home, not sign up for something they don't fully understand.

Northern's family has been part of Central Maine since 1950, and one thing that hasn't changed is this. People want straight answers. They want real sale prices, a no-hassle experience, and financing that feels understandable. For shoppers curious about easy furniture financing options, a soft pull is often the first term worth clearing up.

Table of Contents

- Making a House a Home Without the Worry

- Soft Pulls vs Hard Pulls Explained

- When Soft Pulls Are Used in Your Daily Life

- How We Make Financing Simple at Northern

- Practical Tips for Managing Your Credit Inquiries

- Frequently Asked Questions About Soft Credit Checks

Making a House a Home Without the Worry

In Central Maine, home projects don't always happen all at once. A family might start with the mattress because better sleep can't wait. Then the worn-out recliner goes next. After that, the dining set finally gets replaced so the room feels ready for holidays again.

The hesitation usually shows up right before the decision. Someone finds the right sectional, or a mattress that fits the way they sleep, and then the financing question puts a pause on the whole thing. Plenty of shoppers assume any credit check will dent their score, even before they've decided whether the purchase makes sense.

That's where confusion causes more stress than the financing itself.

Soft pull language sounds technical, but the basic idea is simple. It's a way to check eligibility without turning that first look into a full credit application.

For a local family trying to balance comfort, budget, and timing, that matters. It gives them room to gather information first. They can think through monthly payments, compare options, and decide whether they're ready to move ahead.

Why this matters for Maine households

A home isn't furnished in theory. It's furnished around real life. Kids grow, rooms change, guests stay over, and old furniture eventually stops doing its job.

That's why understanding financing matters just as much as choosing the right fabric, layout, or mattress feel. A shopper shouldn't have to choose between asking a basic question and protecting credit confidence.

A clear explanation helps remove that pressure. Once people understand what is a soft pull credit check, the process usually feels a lot less mysterious and a lot more manageable.

Soft Pulls vs Hard Pulls Explained

A soft pull and a hard pull both involve looking at credit information, but they happen at different stages.

A soft pull credit check is usually used for an early look. It helps answer a simple question. Is this person likely to qualify? Because it is not a formal application for new credit, it does not affect your credit score. A hard pull comes later, when someone submits an actual application for new credit and a lender needs to make a decision. Consumer credit guidance also explains that soft inquiries are generally visible only to the consumer, while hard inquiries can be visible to lenders reviewing a report, as explained in this overview of soft and hard credit inquiries.

For a Central Maine shopper, the difference matters more than the terminology. If you are picking out a mattress for the camp, replacing a worn-out recliner, or furnishing a new place in Waterville, Augusta, or Skowhegan, a soft pull lets you check the road ahead before you commit to the trip.

What the difference looks like in real life

A soft pull is informational. It is similar to walking the showroom floor, checking prices, testing a sofa cushion, and asking, "What might fit my budget each month?"

A hard pull is formal. It is closer to sitting down to complete the application and asking a lender to decide whether to open a new credit account.

That is where confusion usually starts. Both steps involve credit. Only one is tied to the final lending decision.

- Soft pull: used for prequalification, eligibility screening, account review, or other early-stage checks

- Hard pull: used when a person applies for new credit and the lender needs to evaluate the application

- Soft pull visibility: generally stays on the version of the report you see

- Hard pull visibility: can appear to other lenders reviewing your credit

Soft Pull vs Hard Pull At a Glance

| Feature | Soft Pull (Soft Inquiry) | Hard Pull (Hard Inquiry) |

|---|---|---|

| Connection to a credit application | Not attached to a specific new credit application | Tied to a new credit application |

| Effect on credit score | Does not affect credit scores | May affect credit scores |

| Typical visibility | Generally visible only to the consumer | Visible to third parties reviewing the report |

| Common uses | Checking personal credit, background screening, prequalification | Applying for new credit |

A practical way to sort it out is to ask what the check is for. If the goal is to see whether financing could be an option, that is often a soft pull. If the goal is to approve or deny a new credit application, that is often a hard pull.

That is why our no-impact prequalification process feels less stressful for many families. It gives you a chance to get a clearer picture before you decide whether to take the formal next step. If you want more context around store financing language, this guide to buying furniture with no credit check options explains related terms in plain English.

For home furnishing decisions, that breathing room matters. Soft pulls help with planning. Hard pulls come in when it is time for an actual lending decision.

When Soft Pulls Are Used in Your Daily Life

A soft pull sounds unusual until people notice how often it shows up in normal life.

Someone checks their own credit before moving. A company reviews credit information while considering a prescreened offer. An employer includes a credit-related background review for a role where that's part of the hiring process. A current account gets reviewed behind the scenes.

Common places people run into soft pulls

The CFPB notes that soft inquiries are generally visible only to the consumer, while hard inquiries are visible to third parties. It also explains that soft inquiries can include prescreening, employment screening, and reviews of existing accounts, in this consumer explanation of what a credit inquiry means.

That helps explain why a soft pull doesn't always arrive with a big obvious moment attached to it. It can happen as part of routine financial housekeeping.

- Personal credit checks: A person reviews their own report before making a major purchase.

- Prescreened offers: A company checks whether a consumer fits broad criteria for an offer.

- Employment review: Some employers use credit-related background screening where legally permitted.

- Existing account review: A current provider reviews an account as part of ongoing monitoring.

Why this matters when furnishing a home

A shopper looking at monthly furniture payment options is often trying to answer a simple question. Can this purchase fit the household budget without creating new stress?

A soft pull helps with that first question. It gives the shopper room to explore. It also makes financing feel more familiar, because the same type of inquiry already appears in everyday situations outside the furniture store.

That familiarity matters. Once people see soft pulls as a normal tool instead of a warning sign, they usually feel more comfortable taking the first step.

How We Make Financing Simple at Northern

A lot of Central Maine shoppers walk in with the same quiet concern. They want the mattress, sofa, or dining set that will make the house feel finished, but they do not want one early financing step to create new worry.

Why prequalification feels less stressful

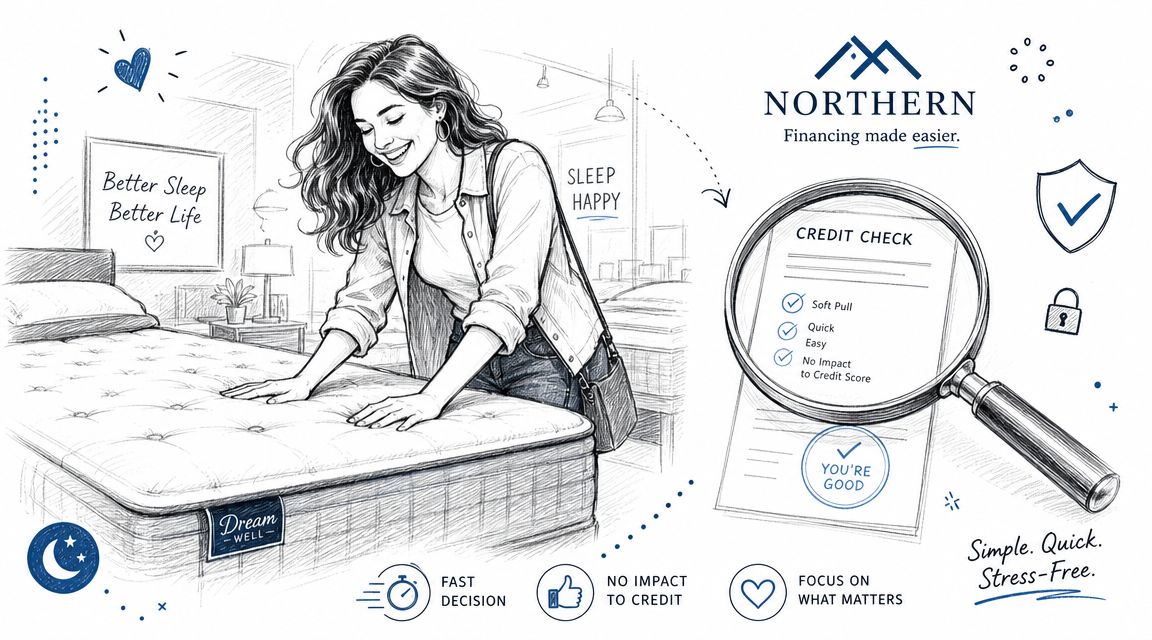

At Northern Mattress & Furniture 1st, the first financing step is meant to answer a simple question. Is this likely to fit before you commit to a full application?

That is why the Nest Credit Card includes a prequalification step that uses a soft pull. In plain terms, it lets shoppers check whether they may qualify without affecting their credit score. It works like checking the depth of the water with one foot before stepping all the way in.

That matters when someone is still deciding. A family in Augusta may be comparing two sectionals that fit the room differently. A couple in Skowhegan may know they need a better mattress now, but still be sorting out the budget for bedroom furniture later. Prequalification gives them useful information early, while the decision is still taking shape.

A no-impact prequalification step gives shoppers room to ask questions first and commit later.

How this fits real home purchases

Furnishing a home is rarely one neat, simple transaction. It is often a mix of comfort, timing, room size, delivery planning, and budget.

A softer first step helps because it lowers the pressure at the beginning.

- For mattress shoppers: It keeps the focus on support, comfort, and sleep quality. People can learn what may be available to them before worrying that a first check will leave a mark on their credit.

- For furniture shoppers: It helps with real side-by-side choices, such as whether a recliner makes more sense now, or whether a living room set better solves the bigger need.

- For custom orders: It gives buyers breathing room while they sort through fabric, layout, and size choices, especially when they are trying to furnish a home thoughtfully instead of rushing to fill a room.

For many households, that first step feels less like an application and more like a budget check. If you want to review our furniture financing options at Northern Mattress & Furniture 1st, that is the practical role prequalification plays. It helps you explore what may work before you decide how to furnish your home.

Practical Tips for Managing Your Credit Inquiries

Understanding soft pulls is useful. Managing credit information with confidence is even better.

Many people stop at one question: will this hurt the score? That's important, but it isn't the whole story. A soft pull can still be a meaningful data event because it involves who looked at the report, what they were reviewing it for, and whether the consumer understood that review was happening.

What to pay attention to on your report

When reading a credit report, shoppers should look beyond the label and ask what the inquiry means in context.

- Check the type: Is it listed as a soft inquiry or a hard inquiry?

- Check the reason: Was it tied to prescreening, employment screening, or an existing account review?

- Check recognition: Does the company name make sense based on recent activity?

- Check timing: Did it appear around the same time as a known application, background review, or prequalification step?

Soft pulls can be a source of confusion. They don't lower scores, but they still say something about how credit information is being used.

The practical issue isn't only score impact. It's also who can see the inquiry and why that review happened.

Questions worth asking before consent

The strongest habit is asking direct questions before agreeing to any financing or screening step.

A shopper can ask:

- Will this be a soft pull or a hard pull?

- Is this prequalification, or is this a full application?

- Who will be able to see the inquiry?

- What is the credit information being used for?

Those questions are especially useful for people who are budgeting carefully or rebuilding credit confidence. Someone exploring furniture financing for bad credit situations doesn't need vague wording. They need plain terms before they consent.

The bigger lesson is simple. A soft pull is usually harmless to the score, but smart shoppers still pay attention. They read, ask, confirm, and keep records. That's how financing stays a tool instead of becoming a source of uncertainty.

Frequently Asked Questions About Soft Credit Checks

A few questions tend to come up after people learn the basics.

Can someone make a decision after a soft pull

Yes. A soft pull can help a company decide whether to send a prescreened offer, whether someone appears to meet broad eligibility standards, or whether to move forward with an early review step.

What a soft pull doesn't do is create a formal lending application by itself. It's an information review, not the final commitment stage.

How many soft pulls are too many

Soft pulls don't affect credit scores, so people generally don't need to panic when they see them. The better question is whether the inquiries make sense.

If the entries match normal activity, such as checking personal credit, prescreened offers, employment screening, or existing account review, that's usually easier to understand. If something looks unfamiliar, it makes sense to look closer and ask questions.

Does prequalifying mean someone has to buy

No. Prequalification is usually just an early check to see what may be available. It helps a shopper gather information.

That can be especially helpful for a household deciding between replacing one item now or doing a larger room update later. A person can review likely financing options and still walk away, sleep on it, or revisit the plan another day.

Can a soft pull still matter if it doesn't hurt the score

Yes. It can matter from a privacy and awareness standpoint.

A lot of people hear “no score impact” and assume “nothing important happened.” That's not always the right takeaway. A soft pull still reflects that someone reviewed credit information for a particular purpose, which is why it's worth understanding the reason behind it.

Is a soft pull useful for home furnishing shoppers

Usually, yes. It's helpful for people who want to plan before they commit.

That includes renters setting up a first apartment, families replacing worn-out pieces, and mattress shoppers focused on improving sleep health rather than rushing into the cheapest option on the floor. When the first financing step is informational, the whole process usually feels more manageable.

For Central Maine shoppers who want a straightforward, no-hassle place to start, Northern Mattress & Furniture 1st offers local guidance, real sale pricing through the Price Chop approach, custom order options beyond the floor models, and simple financing information for households furnishing a home in Augusta, Skowhegan, and nearby communities. Visit the Augusta or Skowhegan showrooms to ask questions in person, browse styles, and enjoy a relaxed shopping experience with complimentary coffee and bottled water.