Blog

Lease Furniture No Credit Check: Central Maine 2026 Guide

A lot of folks in Central Maine hit the same moment. You finally have the apartment, camp, starter house, or downsized place you need. Then you look around and realize you still need a sofa, a bed, a table, maybe a recliner for the room where everyone gathers. The home is there, but it doesn't feel finished yet.

That's usually when credit stress shows up. Maybe your score isn't where you want it. Maybe you've got thin credit, old medical bills, or you just don't want a hard pull while you're juggling a move. When people search lease furniture no credit check, they're usually not looking for something fancy. They're looking for a practical way to make a house feel like home without making a tough month harder.

You're not alone in that. Demand for furniture leasing is growing, and the U.S. market is projected to reach over $13 billion by 2030, according to Grand View Research's United States furniture rental market outlook. That tells you something simple. Many households want flexible ways to furnish their homes when traditional credit isn't the easiest path.

The trouble is that “no credit check” can mean a few very different things. Some options are straightforward. Some are expensive. Some sound better in the ad than they do in the paperwork. If you want a plain-English starting point, this guide to buying furniture with no credit check options is a useful companion.

Table of Contents

- Furnishing Your Maine Home Without the Credit Stress

- Understanding Your No Credit Check Furniture Options

- Weighing the Pros and Cons of Each Path

- Your Step-by-Step Furniture Action Plan

- The Northern Advantage for Maine Families

- Frequently Asked Questions About Furniture Leasing

Furnishing Your Maine Home Without the Credit Stress

In Augusta, Skowhegan, and all across Central Maine, the story is often the same. A family moves in, gets the keys, and spends the first night with takeout on a folding chair or an air mattress. The need is real long before the budget feels comfortable.

I've seen people get confused right at the search stage. They type lease furniture no credit check and assume every result works the same way. It doesn't. One store may offer a lease. Another may offer a soft-pull financing prequalification. A third may suggest layaway. Those are very different roads, even if they all sound easy in a headline.

A young couple might need a basic Ashley living room set now because guests are coming for the holidays. A retired homeowner may need a durable Flexsteel recliner because the old one finally gave out. A parent setting up a child's first apartment may just want something solid, clean, and affordable without a hard inquiry getting in the way.

The best furniture plan isn't the one that gets you approved fastest. It's the one you can live with comfortably after the excitement of delivery day wears off.

That's the heart of this whole topic. Access matters. So does total cost. So does understanding when you own the furniture and what happens if life gets messy for a month or two.

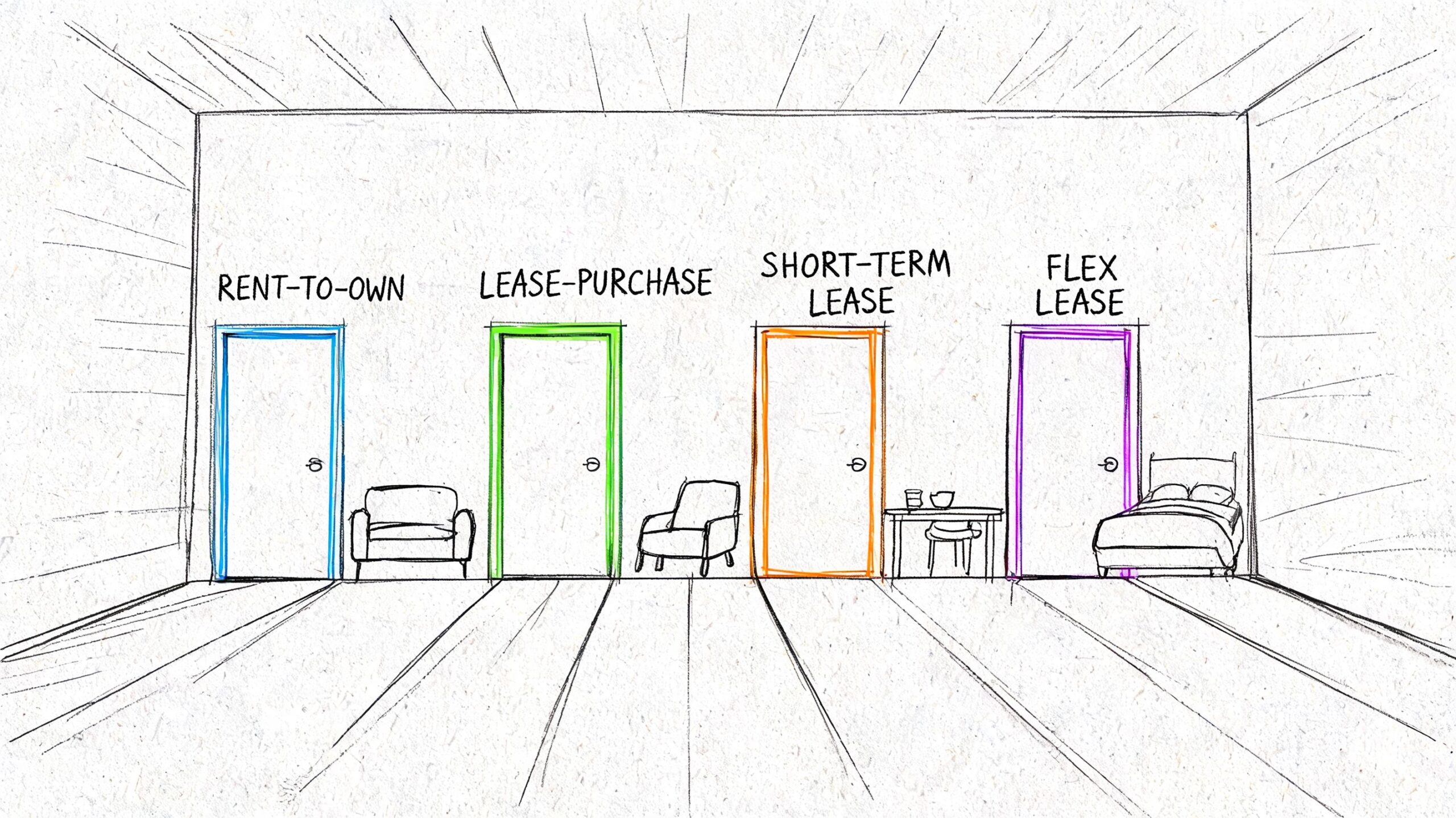

Understanding Your No Credit Check Furniture Options

The phrase no credit check sounds simple, but shoppers usually run into four very different options. Knowing which one you're looking at can save you stress before you ever sit down in a showroom.

What lease to own usually means

A lease-to-own program lets you take the furniture home right away and make scheduled payments over time. You don't fully own the item at the start. Ownership usually comes at the end of the agreement, or through an early payoff option if the contract allows it.

These programs don't rely on a traditional FICO-first approval model. According to Progressive Leasing's explanation of no credit needed approvals, providers use a multi-factor approval process that can look at income, employment, and bank activity, and some providers may approve up to $5,000 based on verifiable income alone. That's why many shoppers with limited credit still get a quick answer.

In plain English, that means they're still checking whether you look stable and real. They're just not using the classic bank-style approval path.

Three other paths people often overlook

A lease isn't your only choice. Many Maine shoppers do better when they compare these alternatives first.

Soft-pull financing: Some stores offer a prequalification process that doesn't impact your credit score. You answer a few questions, get a sense of your options, and then decide whether to move forward. For many people, this is a calmer first step than jumping straight into a lease. A practical example is exploring monthly payments on furniture through a soft-pull prequalification process.

Layaway: Layaway is simple and old-school. You make payments before you bring the furniture home. There's no immediate delivery, but there's also less risk of taking on a payment plan you later regret. This can be a good fit when the need isn't urgent.

Cosigner help: If a trusted family member is willing, a cosigner can sometimes open the door to standard financing terms that are easier on the wallet than a lease. This path needs clear communication because both people take on responsibility.

Here's where readers often get tripped up:

| Option | Take it home right away | Ownership timing | Typical approval style |

|---|---|---|---|

| Lease to own | Yes | Later | Alternative data |

| Soft-pull financing | Often yes | Usually at purchase, subject to terms | Prequalification |

| Layaway | No | After final payment | Store policy |

| Cosigner financing | Often yes | Usually at purchase, subject to terms | Joint application |

Practical rule: If the paperwork says “lease,” read it as a lease first, not as a credit card and not as a traditional installment loan.

That single distinction clears up a lot of confusion.

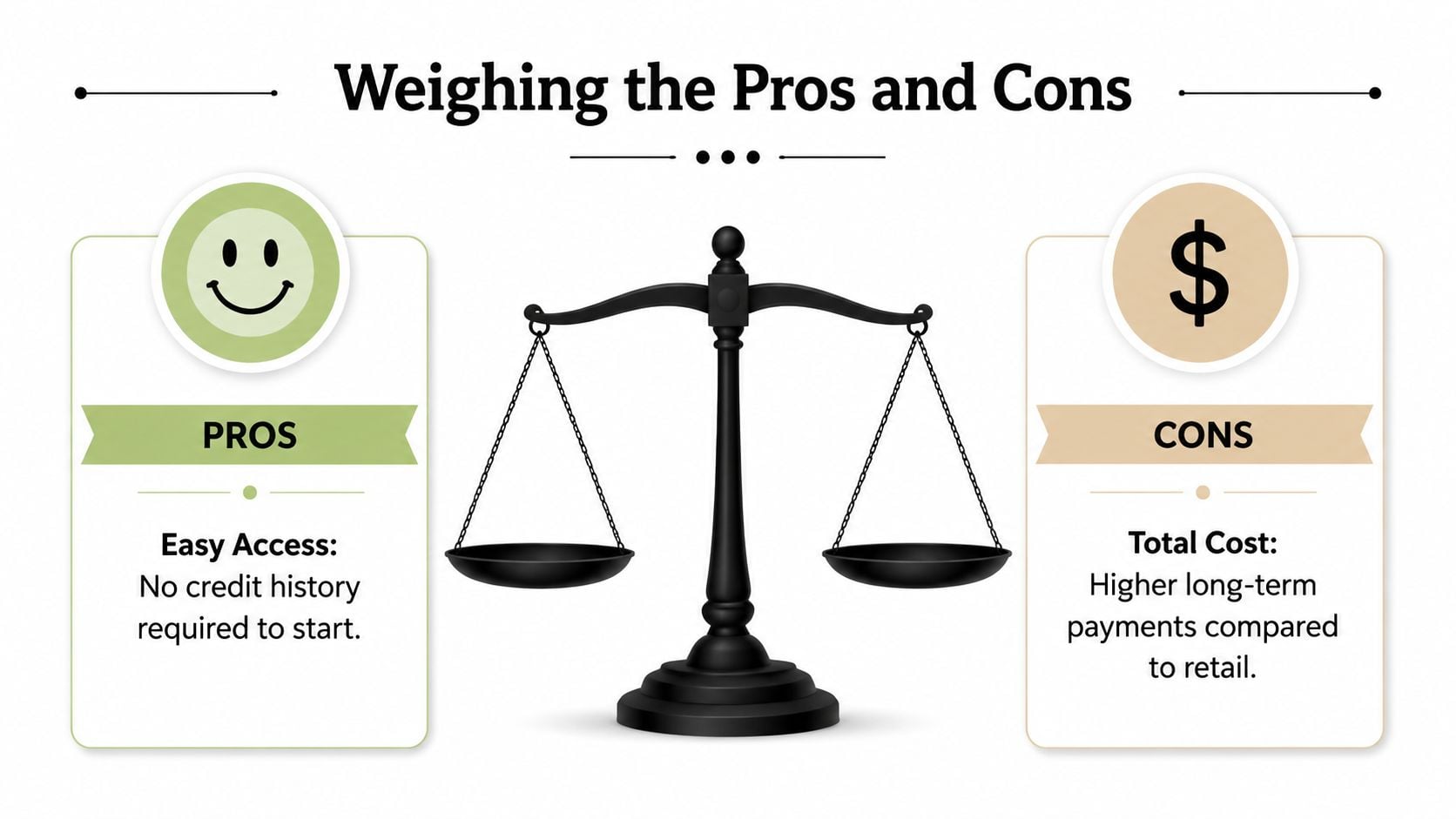

Weighing the Pros and Cons of Each Path

Once you know what each option is, the next question is simple. Which one makes sense for your household, your timing, and your budget?

A simple side by side view

Below is the plain version I'd give a neighbor over coffee.

Lease to own

- Best part: Fast access when traditional credit is a hurdle.

- Watch for: Higher total cost, strict payment terms, and delayed ownership.

- Good fit: You need furniture soon and other doors are closed.

Soft-pull financing

- Best part: You may get clearer terms without starting with a hard inquiry.

- Watch for: Approval still depends on the lender's standards.

- Good fit: You want to compare terms before committing.

Layaway

- Best part: Keeps you from stretching the budget too far.

- Watch for: You don't get the furniture until it's paid.

- Good fit: The purchase can wait and you want maximum control.

Cosigner

- Best part: Can improve access to more affordable financing.

- Watch for: Shared responsibility can strain relationships if payments get difficult.

- Good fit: You have strong family support and clear expectations.

If you're making a larger furniture decision, this broader guide on why furniture purchases are high consideration decisions is worth reading because comfort, durability, and room fit matter just as much as the financing line.

The cost question matters most

Here's the part many ads leave in small print. Consumer analyses summarized by Advance America's furniture financing overview show that lease-to-own programs can cost 2 to 3 times the retail price over a 12 to 36-month term, with effective APRs that can sometimes exceed 100%.

That doesn't mean a lease is automatically wrong. It means you should treat it as a convenience and access tool, not as the default best deal.

If a sofa feels affordable only because the payment sounds small, stop and ask what the full amount will be by the end of the agreement.

That one question changes the conversation.

A durable piece from Ashley or Flexsteel can be a smart investment in your home. But even a good-quality piece becomes a poor value if the financing structure pushes the final cost far beyond what you expected. That's why comparing total obligation matters more than comparing the weekly or monthly payment alone.

Your Step-by-Step Furniture Action Plan

Many individuals do not require additional financing jargon. Instead, they need a clear order of operations. When a steady sequence is followed, the entire process becomes less stressful.

Start with paperwork before you shop

Get your basics together first. That usually means a valid ID, proof of income, your current address information, and anything else a retailer or lease provider may request. If you're shopping with a spouse or partner, have both sets of information ready.

That prep work sounds small, but it keeps you from making a rushed choice just because you're tired of filling out forms in the store.

Use this shopping mindset from the start:

- Know your need: Is this urgent seating, a primary bed, or a dining set you can wait on?

- Know your room: Measure width, depth, and doorways before you fall in love with a sectional.

- Know your comfort priorities: For everyday pieces, durability matters. Fabric, cushion support, and frame quality matter too.

A practical read before you go is this guide on how to shop for furniture smartly.

Use this order when comparing offers

Follow this sequence and you'll usually make a better decision.

- Try a soft-pull prequalification first. If you can review terms without harming your score, start there.

- Ask about store payment options next. Some stores have simpler paths than the big lease ads suggest.

- Use layaway for non-urgent needs. It's slower, but it protects you from overcommitting.

- Review lease-to-own last. If that's the right path for your situation, read every line and ask for the total amount over the full term.

- Check early payoff language carefully. If the agreement offers an early purchase option, make sure you understand how it works and what deadline applies.

Bring a notebook or use your phone. Write down the item price, payment amount, total term, and the final total you'd pay. Seeing those side by side keeps emotion from driving the decision.

That's how you turn a stressful shopping trip into a clear household decision.

The Northern Advantage for Maine Families

Central Maine shoppers are often better served when they start with a calm, transparent option rather than assuming a lease is the only path. That matters even more when you're furnishing several rooms at once or trying to balance a move, utility deposits, and everyday expenses.

Why a soft pull should usually come first

No-credit-needed lease programs can be very accessible. According to Kornerstone Living's guide to no credit needed furniture financing, these programs can have approval rates over 90% for applicants with verifiable income and references. That accessibility is real, and for some households it's useful.

But accessibility alone shouldn't make the decision for you. If you can start with a Nest Credit Card prequalification that doesn't harm your score, that usually gives you a cleaner first look at whether more favorable terms are available. It's a smarter first pass because you're comparing before you commit.

Why lower upfront pricing changes the math

Good financing matters. So does the starting price of the furniture itself.

A third-generation, family-owned retailer that has served Central Maine since 1950, with roots in Augusta and Skowhegan, brings a different mindset than a high-pressure chain ad. Lower “Real Sale Prices,” the Price Chop promise, and a no-hassle showroom experience can reduce the amount you need to finance in the first place. That changes the whole equation.

Add in custom order options for fabrics, sizes, and layouts, and shoppers aren't forced to choose between an expensive special order and a floor sample that doesn't really fit the room. For Maine families trying to make a house a home, that combination matters. So does practical support like free furniture delivery information for local shoppers.

You also want people who'll talk with you plainly. Not just about financing, but about whether a sofa will hold up, whether a recliner fits the room, and whether a custom configuration makes more sense than settling for what's on the floor.

Frequently Asked Questions About Furniture Leasing

The biggest questions usually come up after a shopper has already looked at a lease agreement and started noticing the fine print. Here are the short, honest answers.

Will leasing furniture build my credit

Usually, no. Many no-credit-needed lease programs are designed so they don't operate like a traditional credit card or installment loan. In many cases, they don't help build your score the way people assume.

That confuses a lot of shoppers because the application process still asks for personal and financial information. But giving information for approval isn't the same as building positive credit history through bureau reporting.

If your main goal is credit building, ask that question directly before signing anything. Don't assume the account will help just because you make every payment on time.

What is the difference between no credit check and no credit needed

In everyday conversation, people use those phrases like they mean the same thing. They often don't.

No credit needed usually means the provider is using other information to decide whether to approve you. That can include identity verification, employment, income, and bank activity. You may still go through a screening process, but it isn't centered on your FICO score.

No credit check, in ads, can be much fuzzier. Sometimes it points to a lease structure. Sometimes it's just broad marketing language. That's why the contract matters more than the headline. If the agreement says lease, treat it like a lease. If it says revolving credit or installment financing, read it through that lens instead.

What happens if I can't keep up with payments

This is the question people should ask before delivery, not after.

With a lease-to-own agreement, you may not fully own the furniture yet. If payments become unaffordable, the provider may have rights under the contract that are different from ordinary store financing. That can include taking back the merchandise, ending the agreement, or applying fees based on the terms you accepted.

A few simple habits can protect you:

- Read the payment schedule closely: Know the due dates and the amount due each time.

- Ask about hardship options: Some providers may offer a pause or alternative arrangement, but you need to ask before missing multiple payments.

- Keep your paperwork: Save the agreement, receipts, and payoff details.

- Don't shop by payment alone: Small payments can hide a much larger total obligation.

Furniture should support your life, not keep you up at night. Whether you're looking at a sectional, a bedroom set, or a mattress to improve sleep health, the right fit is about comfort, durability, and a payment structure you can manage with confidence.

If you'd like neighborly guidance without pressure, Northern Mattress & Furniture 1st is a solid place to start. Visit the Augusta or Skowhegan showrooms, grab a coffee or bottled water, and talk through your options with a team that's been helping Central Maine families since 1950. If you want flexible terms, custom order choices, real sale pricing, or a soft-pull Nest prequalification, they'll help you find the right fit for your home.