Blog

Monthly Payments on Furniture: A Central Maine Guide

A lot of furniture decisions happen the same way in Central Maine. You move into a new place, or you finally decide the old sofa has done its time, or you realize that the dining set you’ve been “making work” isn’t really working at all. You want something better. You also want to keep your savings intact for oil, groceries, repairs, and everything else real life throws at a Maine household.

That’s where monthly payments on furniture can make good sense. Instead of settling for a piece you don’t love or draining cash all at once, you spread the cost into payments that fit the rest of your budget. And you’re far from alone. According to a 2022 Provoke Insights survey of recent furniture buyers, 30% of U.S. consumers who bought furniture in the last year used a financing option.

For a third-generation family business serving Augusta, Skowhegan, and the surrounding area since 1950, that shift isn’t surprising. Families still want durability. They still care about value. They just want a simpler path to making a house feel finished and comfortable.

Table of Contents

- Furnishing Your Maine Home The Smart Way

- How Furniture Financing Actually Works

- The Different Types of Payment Plans

- Simple Financing with the Nest Credit Card

- A Sample Monthly Payment Calculator

- Smart Tips to Lower Your Monthly Payments

- Common Financing Pitfalls and How to Avoid Them

- Your Central Maine Furniture Financing Questions

Furnishing Your Maine Home The Smart Way

When timing and budget collide

In this part of Maine, home tends to matter more as the seasons turn. Summer guests come through. Fall evenings get longer. By the time winter settles in, you feel every inch of your living room, bedroom, and dining space. If the recliner sags, the mattress leaves you stiff, or the kitchen table is too small for the way your family lives, you notice it fast.

People don’t generally replace furniture because they woke up one morning eager to spend money. They replace it because life changed. Maybe the kids got bigger. Maybe you downsized. Maybe you bought your first place in Augusta or found a rental in the Skowhegan area that finally feels worth setting up properly.

That’s why monthly payments on furniture are less about “buying more” and more about buying at the right time. If the right sectional, a sturdier bed, or a better dining set improves how your home functions now, waiting years to pay cash isn’t always the smartest move.

Practical rule: If a furniture purchase will improve daily comfort, sleep, storage, or how your family uses the room, it deserves a real budget plan instead of a last-minute compromise.

What monthly payments really change

The biggest shift financing creates is simple. It changes the question from “Can I afford this all at once?” to “Can I handle this comfortably each month?” For many households, that opens the door to better-built pieces from names people already trust, like Flexsteel or Ashley, instead of buying the cheapest option twice.

That can be especially useful if you’re also thinking about custom order choices. A different fabric, a better layout for a sectional, or a dining set sized for your room can make your home feel finished instead of temporary. If you want to shop more thoughtfully, Northern’s guide on how to shop for furniture smartly is a helpful place to start.

A family-owned store that’s been part of Central Maine since 1950 has seen this firsthand. People aren’t looking for complexity. They want clear choices, real sale prices, and a no-hassle way to bring home furniture that lasts.

Here’s the plain truth. Monthly payments work well when they help you buy durable furniture with a payoff plan you can follow. They work poorly when they tempt you into stretching beyond what your monthly budget can support.

How Furniture Financing Actually Works

The three numbers that matter

Furniture financing sounds more complicated than it is. At the counter or online, it usually comes down to three numbers.

- Principal means the amount you’re financing. That’s the price of the furniture purchase after any down payment.

- Term means how long you have to pay it back. The term might be short, or it might stretch longer to lower the payment.

- APR means the annual percentage rate. That’s the interest rate tied to the balance if the plan charges interest.

If you understand those three things, you can sort through most offers without much trouble. A good financing conversation should feel a lot like any other careful buying decision. You compare the total, the timeline, and what the monthly bill will feel like in real life.

A simple example in plain English

Here’s the easiest way to think about it. Say a sofa costs $2,000 and the financing is set at 15% APR over 12 months. According to McElheran’s example of furniture financing math, the first month’s interest is $25, and after you make that payment, the balance drops, so the next month’s interest is slightly lower.

That matters because interest is tied to the remaining balance, not the original sticker forever. Each payment chips away at what you owe. Over time, more of your payment goes toward the furniture itself and less goes toward interest.

A payment plan gets easier to understand once you stop looking at it as one big number and start seeing it as a shrinking balance.

When you’re comparing options, ask these questions:

- What amount am I financing?

- How long is the term?

- Is the APR promotional, standard, or deferred?

- What monthly payment keeps me on track to finish on time?

If you want a broader look at how people move from browsing to buying, this article on the furniture buying journey from first research to final decision lays it out in a very practical way.

The goal isn’t to memorize formulas. It’s to know enough to ask better questions before you sign.

The Different Types of Payment Plans

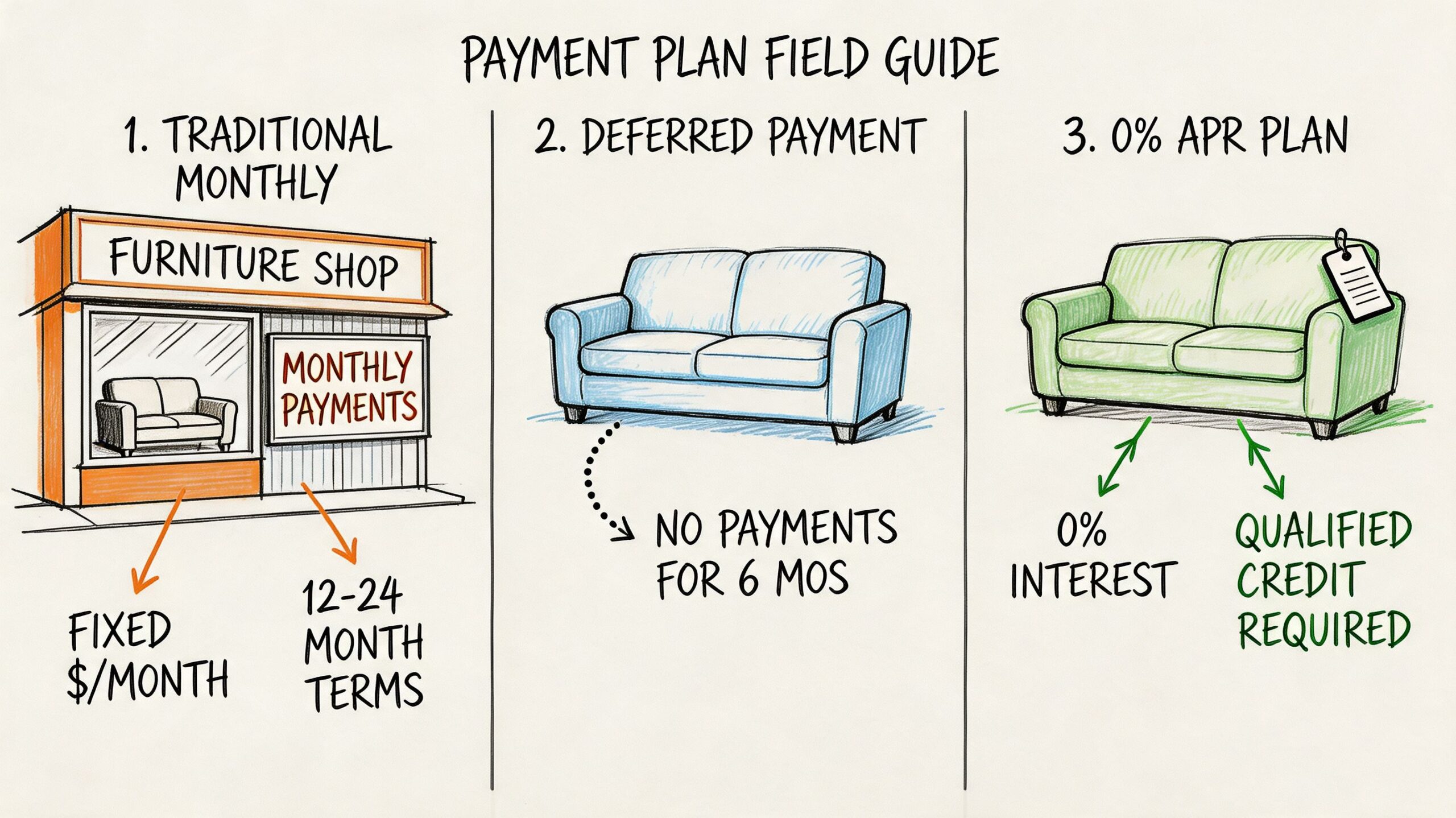

Store cards and promotional financing

Most monthly payments on furniture fall into a few familiar buckets. The first is the traditional store card. This is often the most straightforward option for larger furniture purchases because it’s built for home goods, not just quick checkout convenience.

Store-card financing often gives you promotional periods and fixed monthly planning. That can work well for a full room package, a mattress and adjustable base, or a custom sofa where you want a little breathing room in the budget. It can also make sense if you want one place to track statements and payments.

The upside is structure. The caution is that you need to know whether the promotion is simple interest, standard APR, or deferred interest. That distinction matters a lot, and it’s where many shoppers need clearer explanations.

BNPL and lease-to-own

The second category is Buy Now Pay Later, usually shortened to BNPL. This tends to feel fast and familiar because people see it all over online checkout. According to Furniture Today’s report on BNPL in furniture, Klarna’s Pay in 4 accounts for 80% of furniture-related BNPL transactions, and those plans split purchases into four interest-free bi-weekly payments. The same report notes that longer-term plans can carry APRs up to 35.99%.

That makes BNPL a mixed bag. For a smaller purchase with a short payoff window, it can be simple. For bigger-ticket furniture, the longer-term versions deserve the same careful reading you’d give any credit offer.

Then there’s lease-to-own. This option usually attracts shoppers who want very low barriers up front. It can help when traditional approval is difficult, but it often carries the highest overall cost and different ownership rules. In practical terms, it’s usually the option to examine most skeptically.

A quick way to compare them:

| Plan type | Best fit | Watch for |

|---|---|---|

| Store card | Larger furniture purchases and planned payoff | Promo details and what happens after the promo |

| BNPL | Smaller or shorter-term purchases | Higher APR on longer terms |

| Lease-to-own | Limited credit access | Higher total cost and ownership terms |

If you’re considering custom upholstery, wood species, or configuration choices, this overview of getting started with custom order furniture is useful because payment planning matters more once you move beyond stock floor pieces.

Simple Financing with the Nest Credit Card

Why soft pull prequalification matters

A lot of shoppers hesitate before they even ask about financing. It’s not always the payment itself. It’s the worry that checking options will hurt their credit or lock them into something before they’re ready.

That’s where a simpler process helps. The Nest Credit Card offers a way to pre-qualify without a credit score impact, which removes much of the guesswork at the start. For many people, that’s the difference between exploring a payment option calmly and avoiding the conversation altogether.

That no-impact prequalification is useful when you’re still comparing pieces, deciding between in-stock and custom order, or trying to balance furniture needs with the rest of your monthly obligations. It gives you a clearer lane before you commit.

The best financing tool is the one that lets you understand your options before the pressure kicks in.

Who it tends to fit well

This kind of setup often fits shoppers who want monthly payments on furniture without turning the process into a project. Maybe you’re furnishing a bedroom all at once. Maybe you’re replacing a worn-out recliner and loveseat with something sturdier. Maybe you’ve found the right sectional, but you want the monthly number to be predictable before you move ahead.

Northern Mattress & Furniture 1st offers the Nest Credit Card with that soft-pull prequalification, promotional financing periods, and online account management. In practice, that means shoppers can check eligibility, review terms, and decide whether the payment fits before moving forward.

That’s a sensible path for people who like clarity. It also fits the no-hassle showroom style many Central Maine shoppers prefer. You can ask questions, compare fabrics or brands, and sort out the financial side without feeling boxed in.

For neighbors who care about real sale prices, custom order flexibility, and a straightforward payment option, that combination is often more useful than flashy financing language.

A Sample Monthly Payment Calculator

A payment calculator doesn’t need to be fancy to be helpful. What matters is seeing how the term and APR push the monthly number up or down.

For this example, use a $2,500 furniture purchase. The exact payment will depend on the lender’s terms and how interest is applied, but this layout gives you a practical way to compare offers side by side.

How to read the table

If you look down the 0% APR column, you’ll notice the cleanest math. You’re dividing the purchase by the number of months, with no interest added during the promotional period. As the APR rises, the payment goes up and more of each monthly bill goes toward borrowing cost instead of the furniture itself.

| Estimated Monthly Payments on a $2,500 Purchase | |||

|---|---|---|---|

| Financing Term | 0% APR Promotional | 9.99% APR | 19.99% APR |

| Shorter term | Lower total cost, higher monthly payment | Payment rises with interest | Payment rises more sharply |

| Medium term | Lower monthly payment than short term | More interest over time | Noticeably more total cost |

| Longer term | Lowest monthly payment | Lower payment, more paid overall | Lowest payment, highest borrowing cost |

This is the trade-off in plain language. Shorter terms usually cost less overall. Longer terms usually feel easier month to month. Promotional 0% periods can be the sweet spot if you know you can finish within the window.

If you’re sitting in a showroom deciding between two sofas, this kind of simple comparison can keep you grounded. It also helps you separate “Can I make this work today?” from “Will I still be happy with this payment six months from now?”

Smart Tips to Lower Your Monthly Payments

Start with the amount you finance

The surest way to lower a payment is to finance less in the first place. That sounds obvious, but it’s where many good buying decisions begin.

A few practical moves make a real difference:

- Use promotional financing carefully: If you qualify for a true promotional period and can pay it off on schedule, more of your money goes toward the furniture instead of interest.

- Put money down when you can: Even a modest down payment shrinks the balance you’re carrying month to month.

- Shop from real sale prices: If the starting price is honest, the financed amount is easier to live with.

That last point matters. A lower purchase price doesn’t just save money on day one. It reduces every payment that follows. That’s why Price Chop pricing and real sale pricing matter more than flashy markdown language.

Match the plan to your real life

The second smart move is choosing a payment structure that fits how your household works. If your budget is steady and you want the furniture paid off quickly, a shorter term may be comfortable. If your expenses swing with the season, a little more time may make the payment easier to absorb.

Use this checklist before you say yes:

- Look at your true monthly margin: Don’t use your best month as the standard.

- Plan around other home costs: Heat, car repairs, school expenses, and groceries all compete with furniture payments.

- Choose durability over impulse: A better-built sofa or mattress usually feels smarter than replacing a cheaper one too soon.

- Read up before shopping: Northern’s article on the dos and don’ts of furniture shopping is a solid guide if you want to avoid common mistakes.

Buy furniture with the same mindset you’d use for boots, tires, or a good winter coat. Price matters, but staying power matters more.

For families furnishing a whole room, the smartest monthly payments on furniture usually come from a combination of fair pricing, a realistic term, and a payoff plan you’ve already tested against your regular bills.

Common Financing Pitfalls and How to Avoid Them

The fine print that trips people up

The biggest mistake people make with furniture financing isn’t choosing monthly payments. It’s assuming all “no interest” offers mean the same thing.

Some promotions are straightforward. Others use deferred interest, which means if the balance isn’t paid in full by the end of the promotional period, interest can be charged based on the earlier purchase terms. That can turn a manageable plan into a much more expensive one.

The risk is real because many shoppers carry store-card balances longer than they expected. According to information citing the CFPB on Bob’s financing options page, 75% of store card users carry balances month to month, often with standard APRs in the 28% to 30% range.

That doesn’t mean financing is bad. It means the terms matter. A lot.

Safer habits before you sign

Good habits remove most of the danger. The trick is to treat the promotion like a deadline, not a suggestion.

- Read the exact payoff requirement: Look for language about deferred interest, promo expiration, and what counts as paid in full.

- Divide the balance by the promotional months: That gives you your actual monthly target, not the minimum payment.

- Set calendar reminders early: Don’t wait until the final month to check your progress.

- Ask someone to explain the wording plainly: If the terms aren’t clear, keep asking.

A product description can sound clear while the financing details stay fuzzy, so it helps to build the habit of careful reading across the whole purchase. This guide on how to read furniture product descriptions and buy with confidence can sharpen that skill.

If you can’t explain the payment plan back to someone else in one minute, pause before signing.

The safest financing choice is usually the one you understand completely, with enough room in your monthly budget that one rough month won’t throw the whole plan off course.

Your Central Maine Furniture Financing Questions

Can financing help me buy better quality

Yes, often it can. Better upholstery, stronger frames, and more durable mattresses usually cost more up front, but they can be easier to reach when the purchase is spread into manageable payments. According to HomeSource Systems on consumer finance for furniture retailers, retailers who integrate financing options can see average ticket size rise by as much as 61%, which shows how monthly budgeting can help shoppers feel comfortable choosing higher-quality pieces.

That doesn’t mean spending carelessly. It means you may not have to settle for the first low-price option if a sturdier one fits your monthly plan.

Do I need to choose only what is on the floor

Not at all. One of the better parts of shopping locally is that the floor is often a starting point, not the full menu. If you need a different fabric, layout, finish, or configuration, custom ordering may be available through brands like Flexsteel or Trailways Amish.

That matters because the right fit for your room is often not the exact sample you first sit on. Good financing can make those more personalized choices easier to manage without forcing a cash-only decision.

Should I shop in person if I have questions

If you’re unsure about terms, comfort, construction, or room fit, yes. It’s easier to compare fabrics, test seat depth, and ask direct financing questions in person than it is from a phone screen. It also helps to sit on a sofa, open the drawers, or lie on a mattress before making a bigger home purchase.

For many Maine families, the ideal shopping experience is still a calm one. No hassle. Real answers. Coffee and bottled water nearby. That kind of setting makes it easier to slow down and make a sound decision for your home.

If you’re weighing monthly payments on furniture and want a clear, neighborly conversation about what fits your budget, visit Northern Mattress & Furniture 1st. Stop by the Augusta or Skowhegan showrooms, look at in-stock and custom-order options, and ask about simple financing with no-impact prequalification.